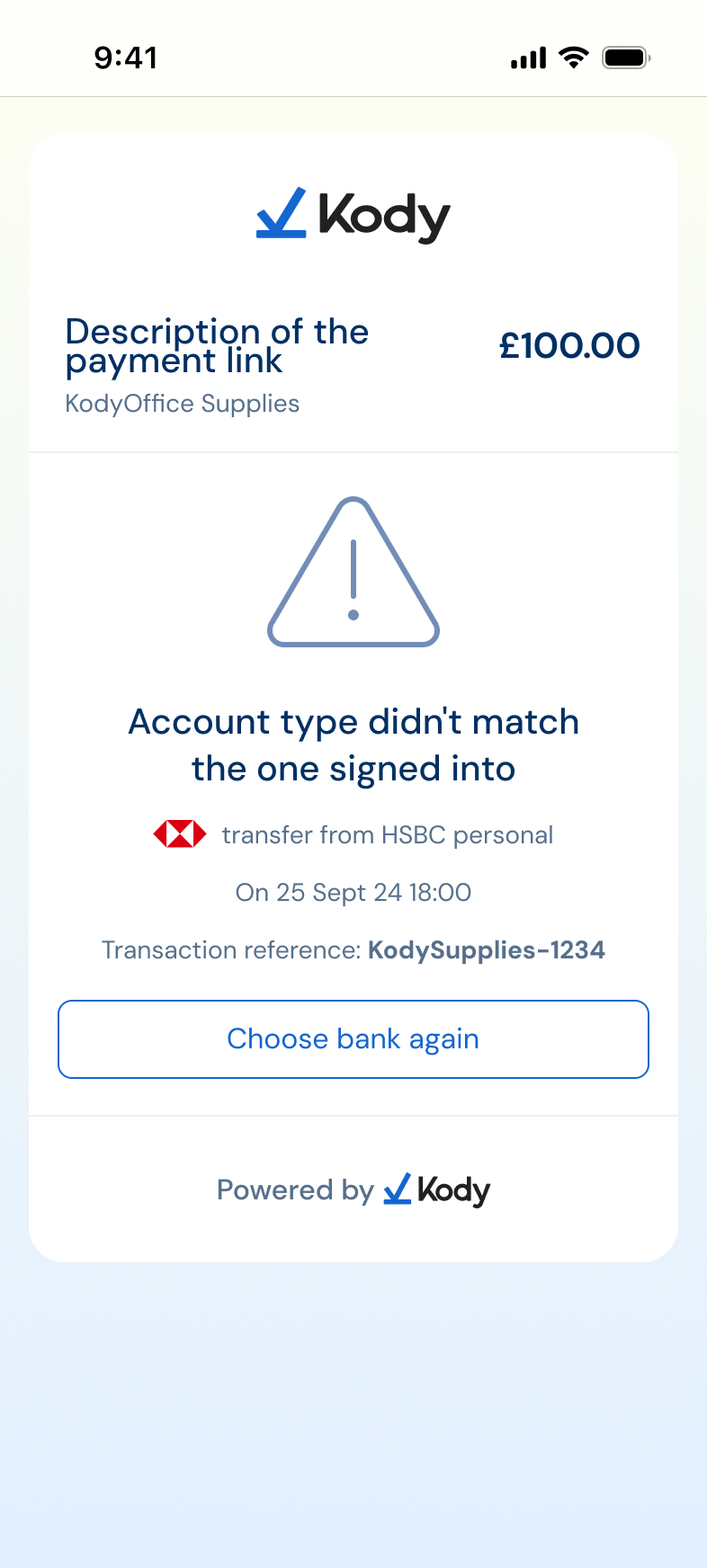

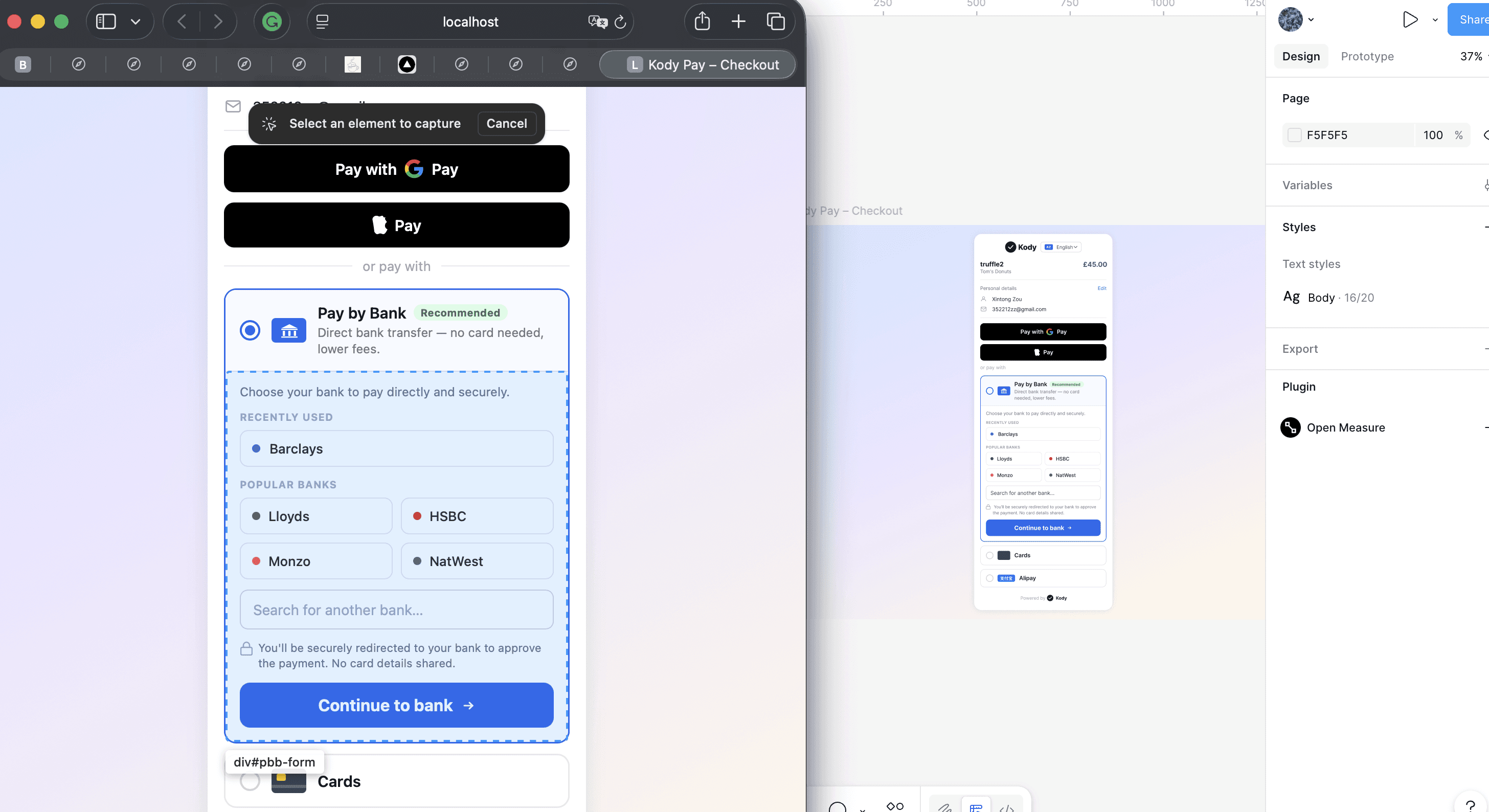

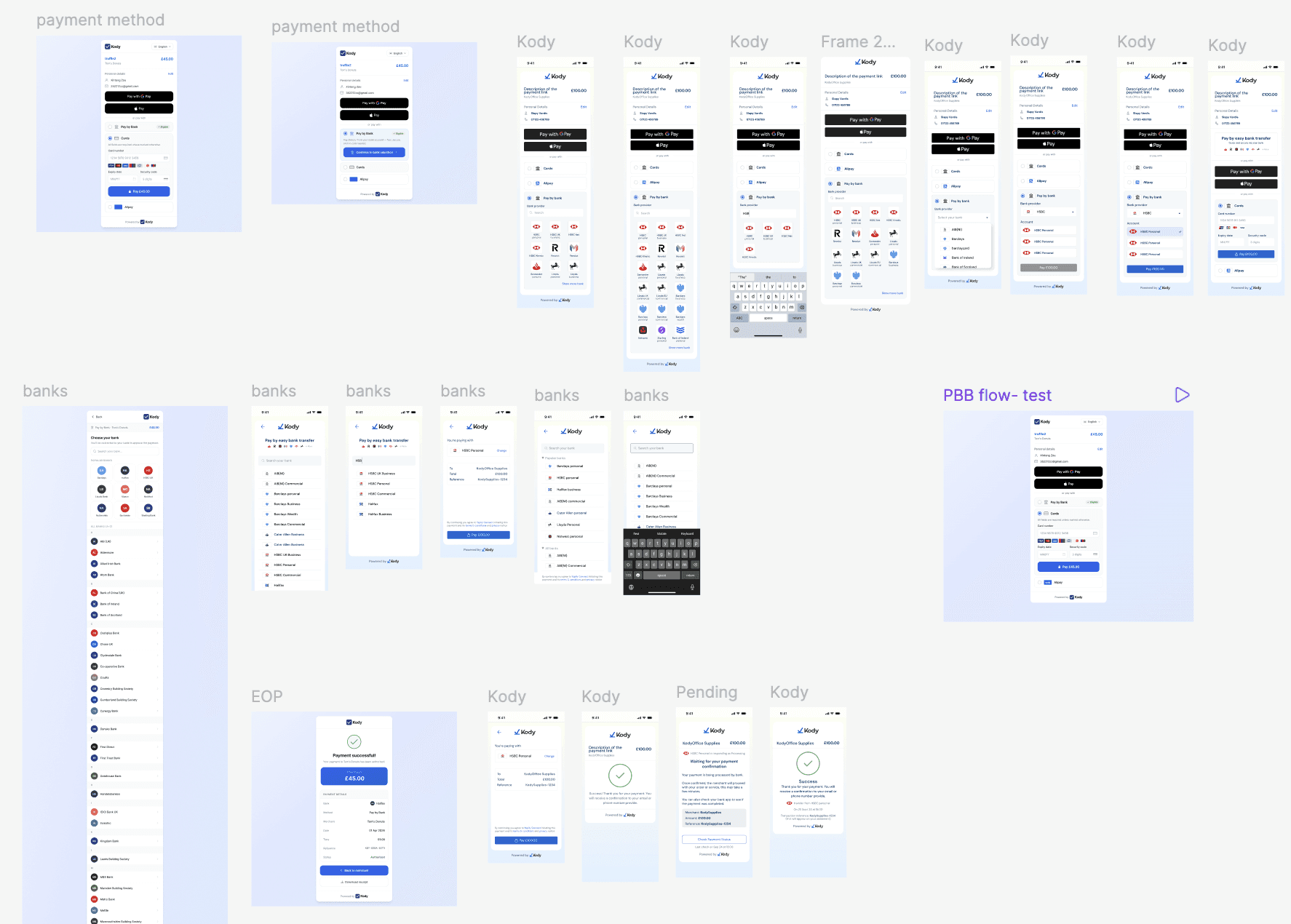

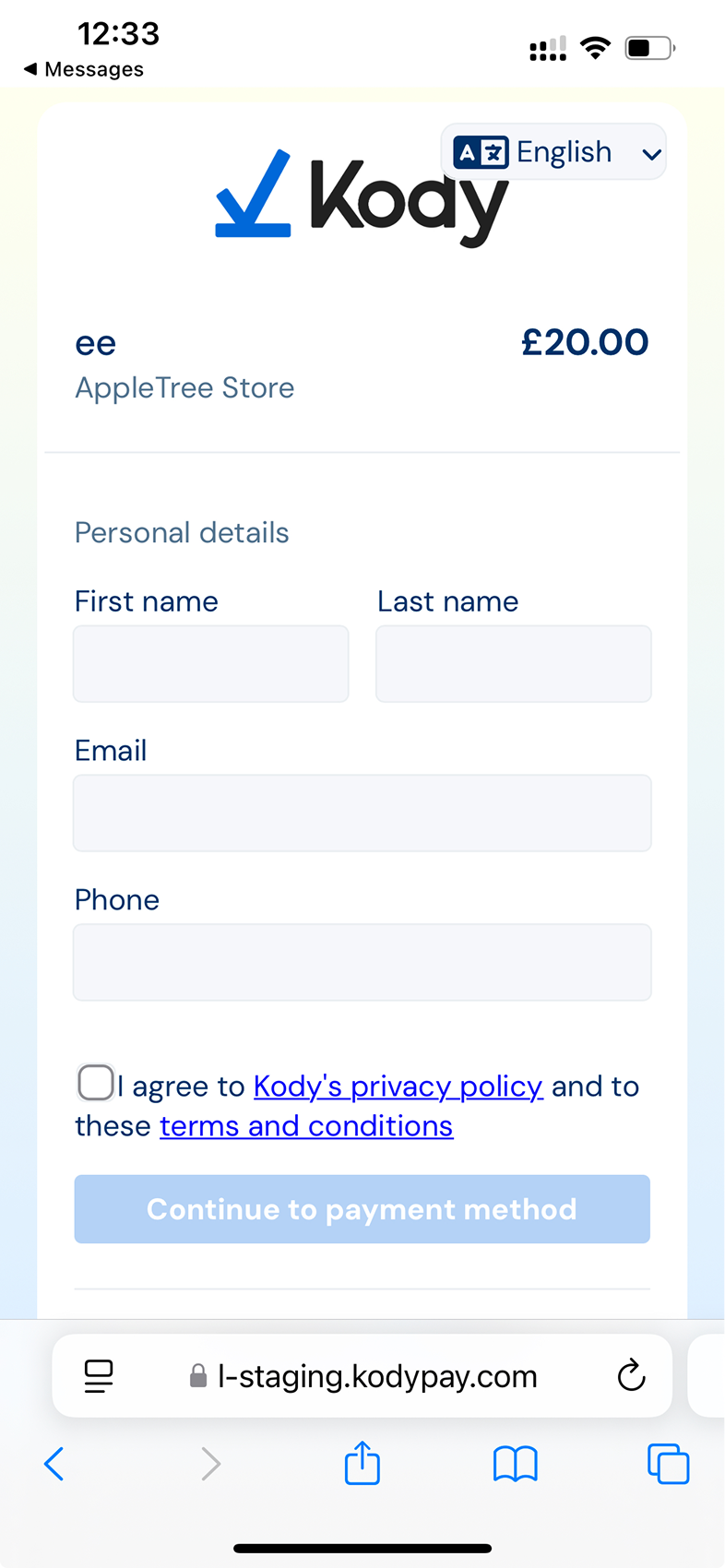

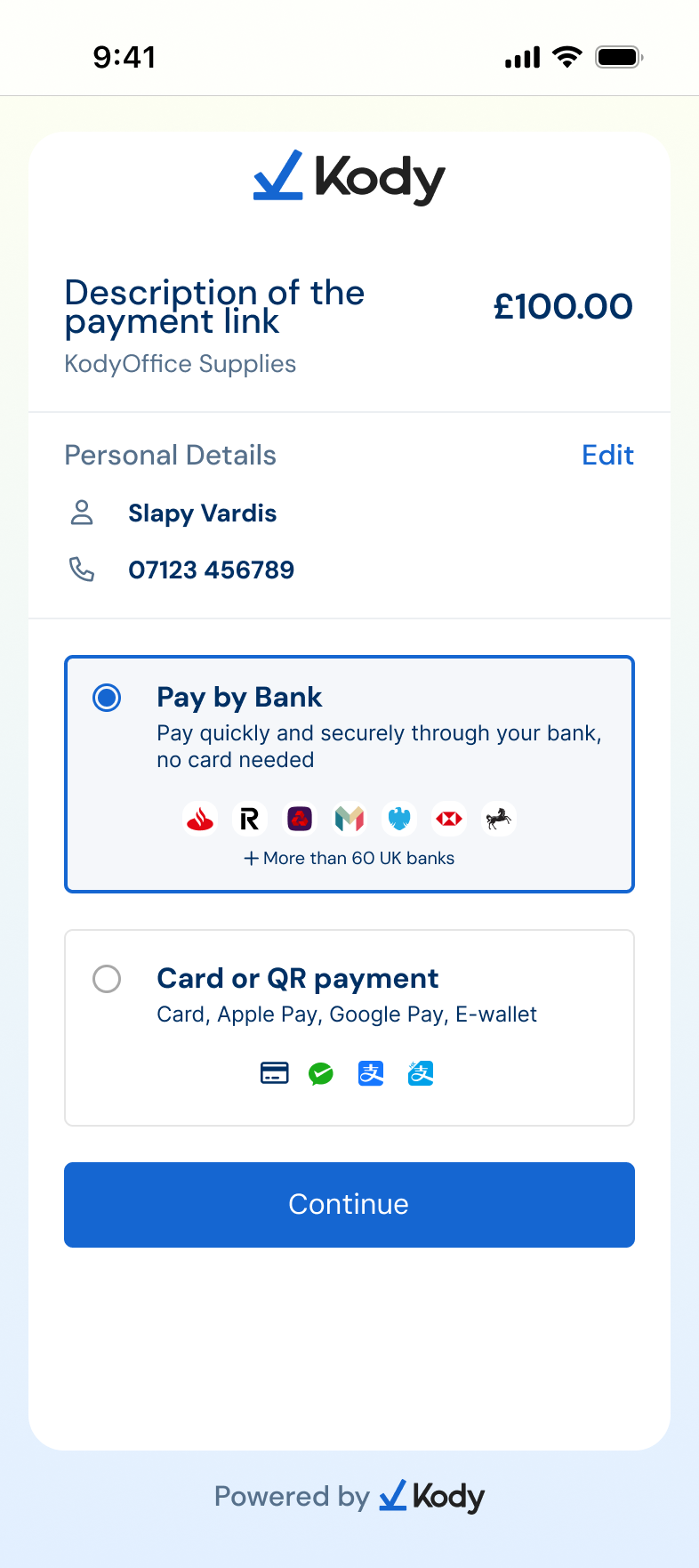

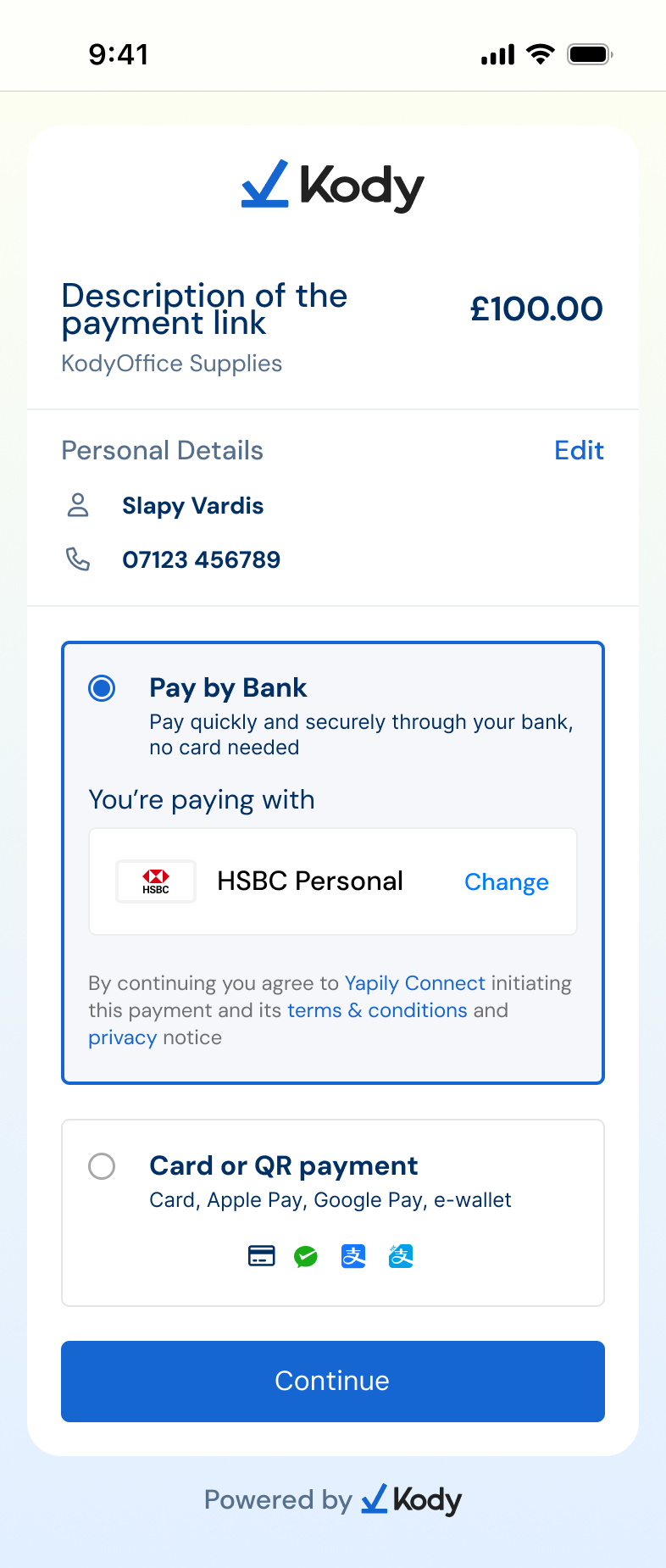

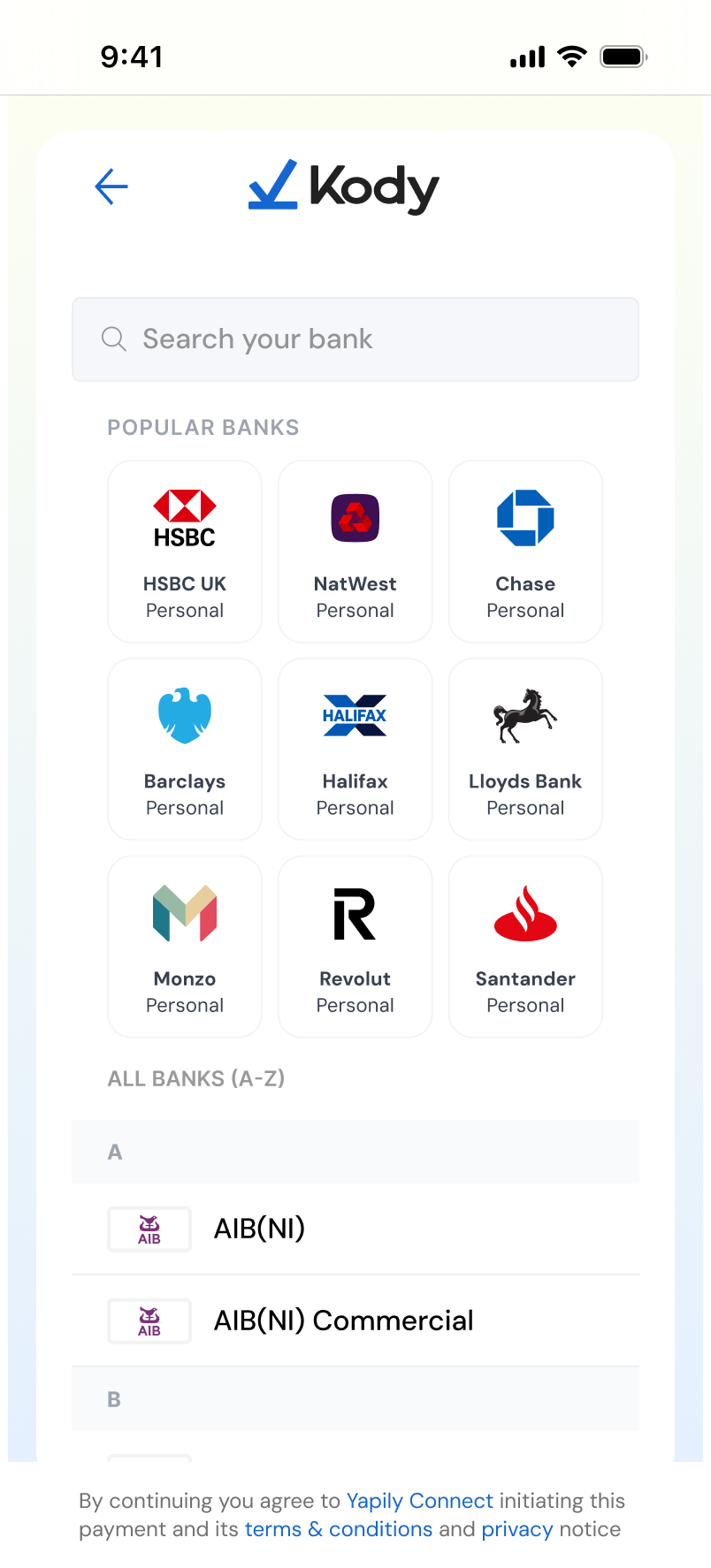

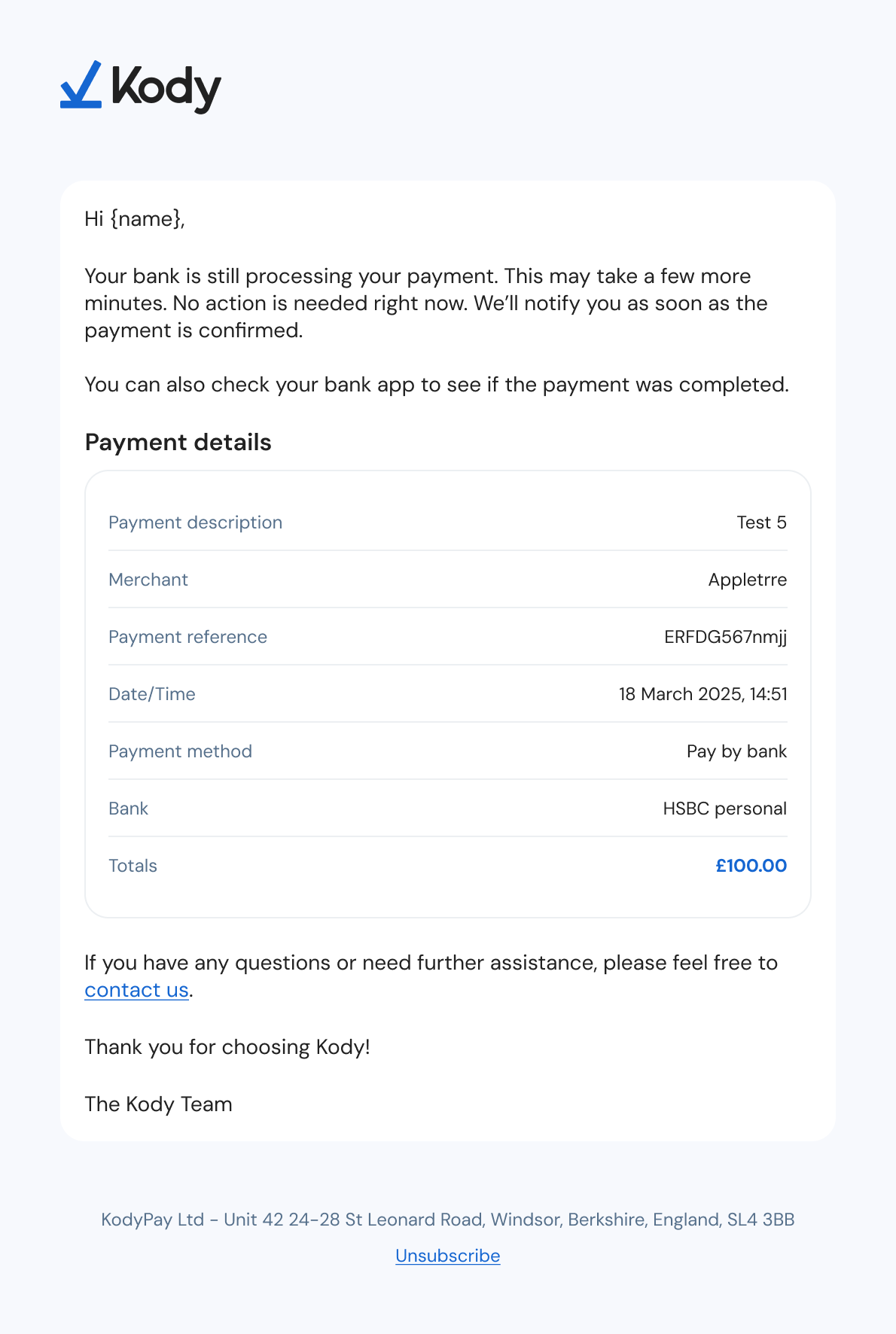

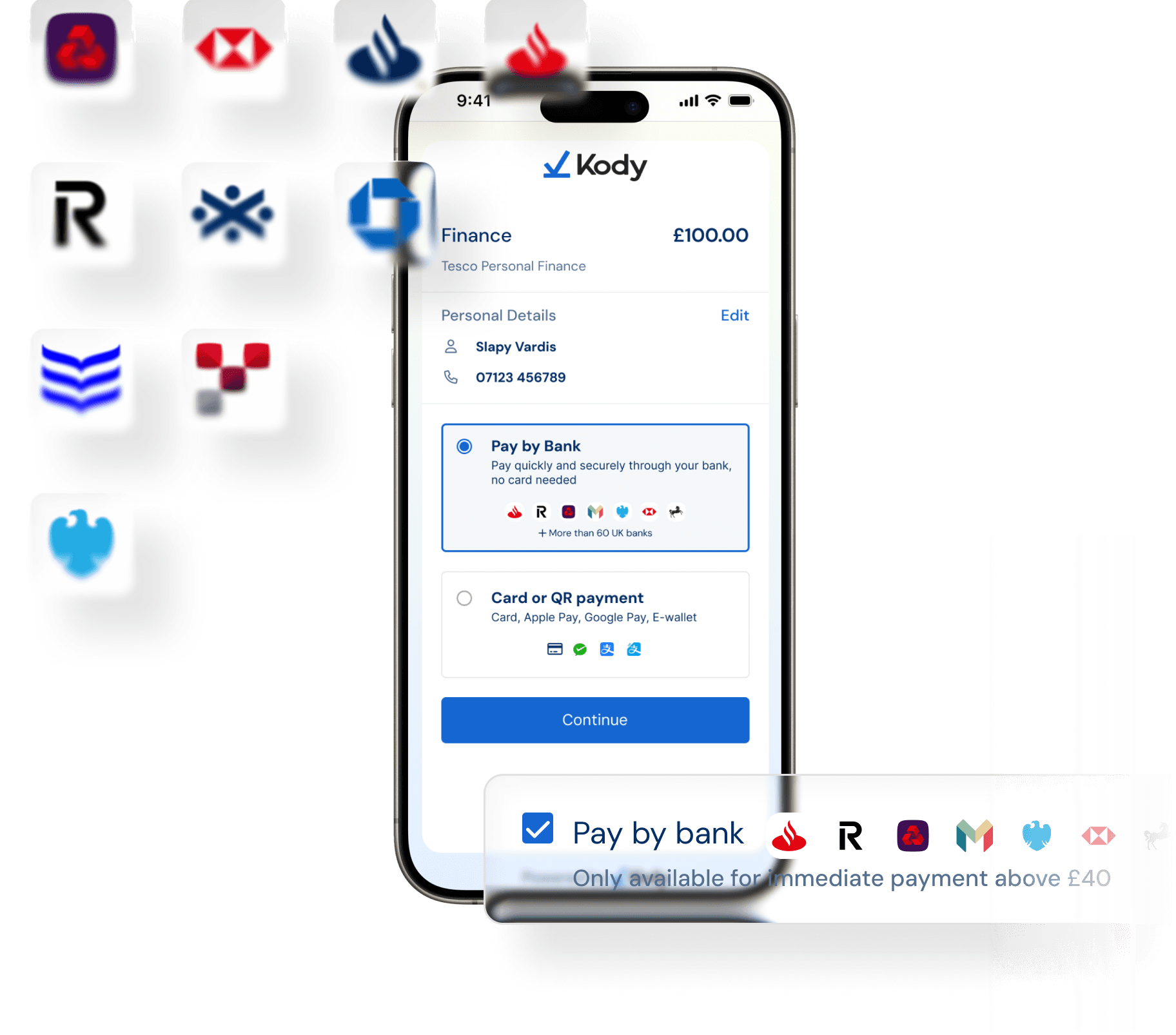

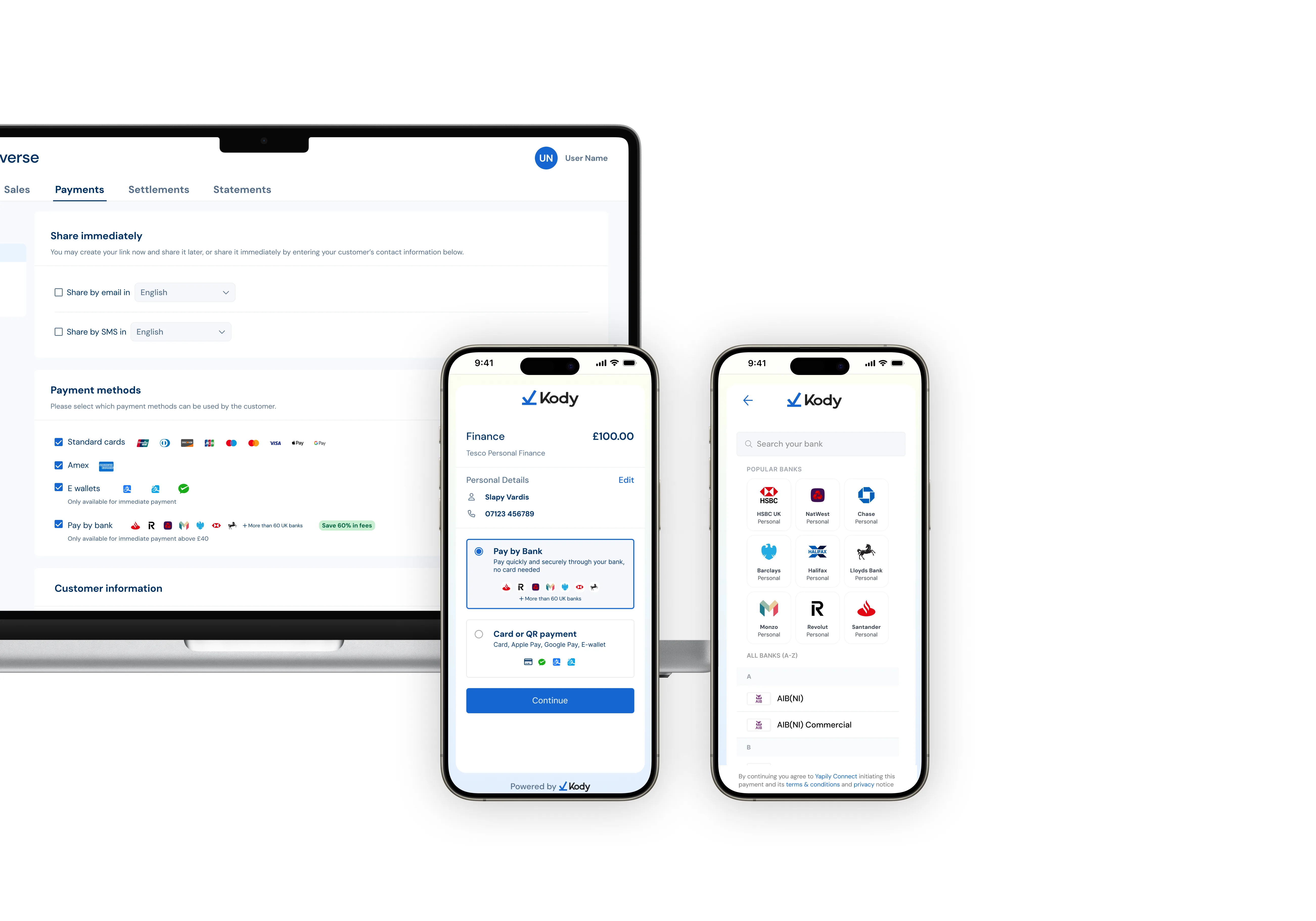

Pay by Bank in Pay by Link

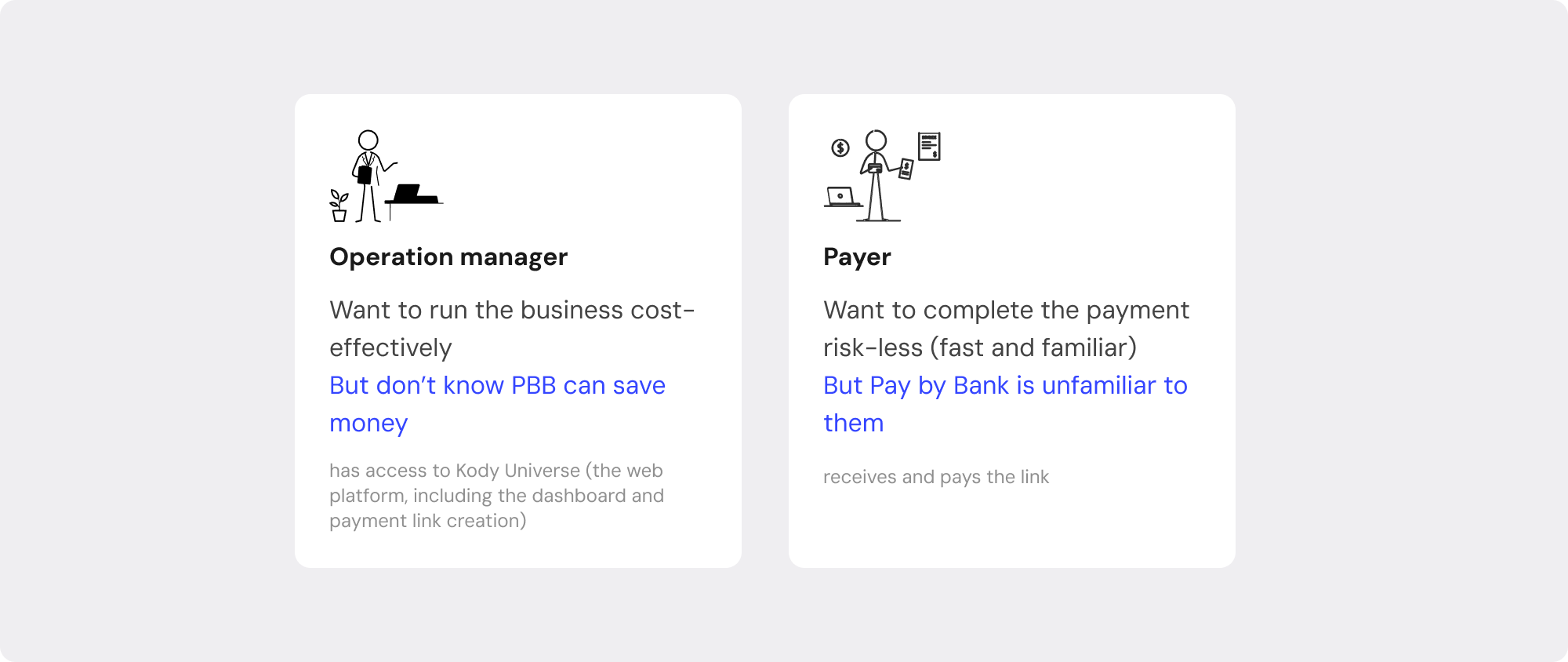

Designing Pay by Bank's integration into Kody's Pay by Link channel, designed for a merchant who does not know it saves money and a payer who never thinks to choose it.

This case covers the design work after Pay by Bank moved to the Pay by Link channel. Check Case A to read how I contributed to the strategic pivot.

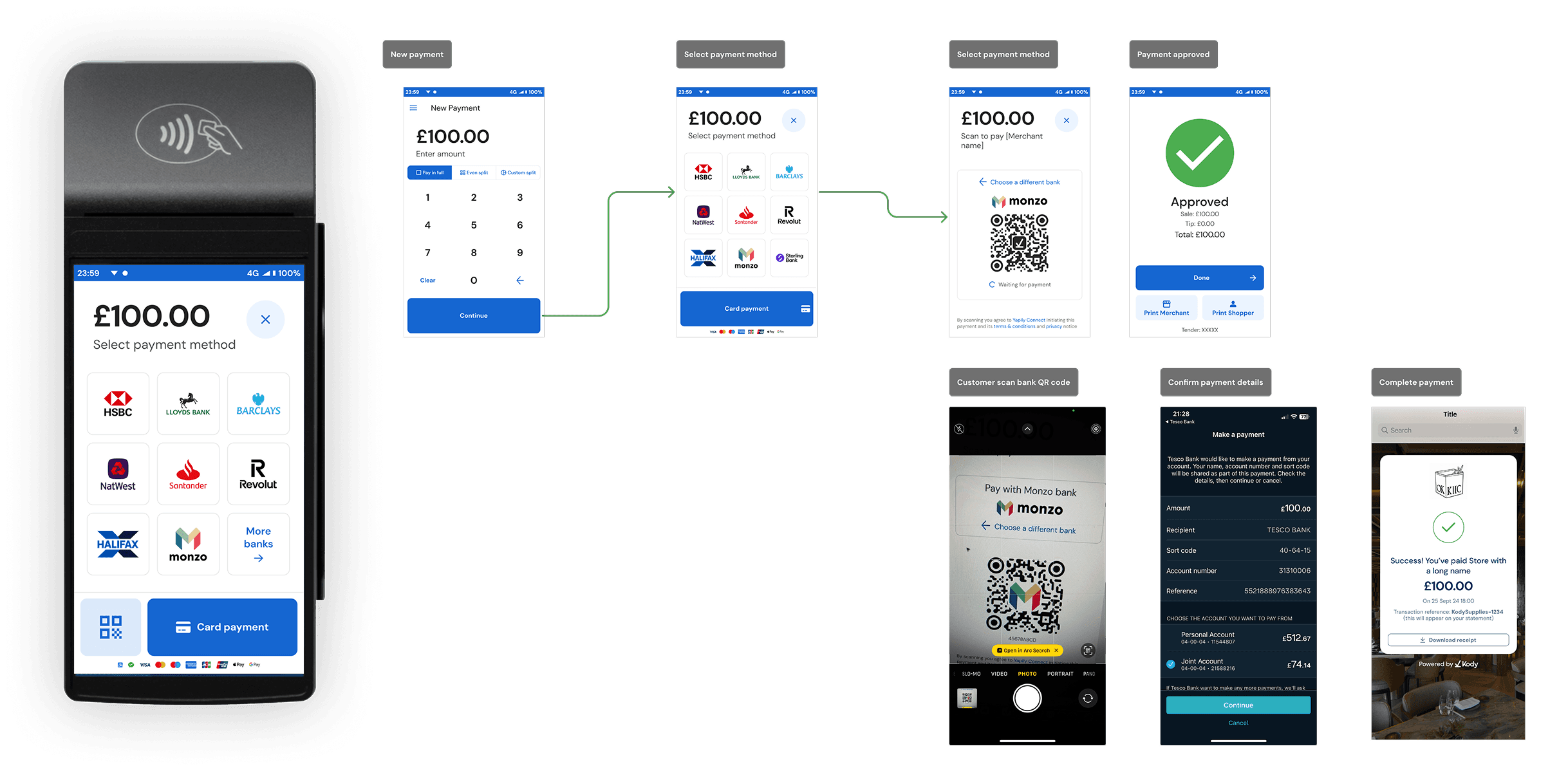

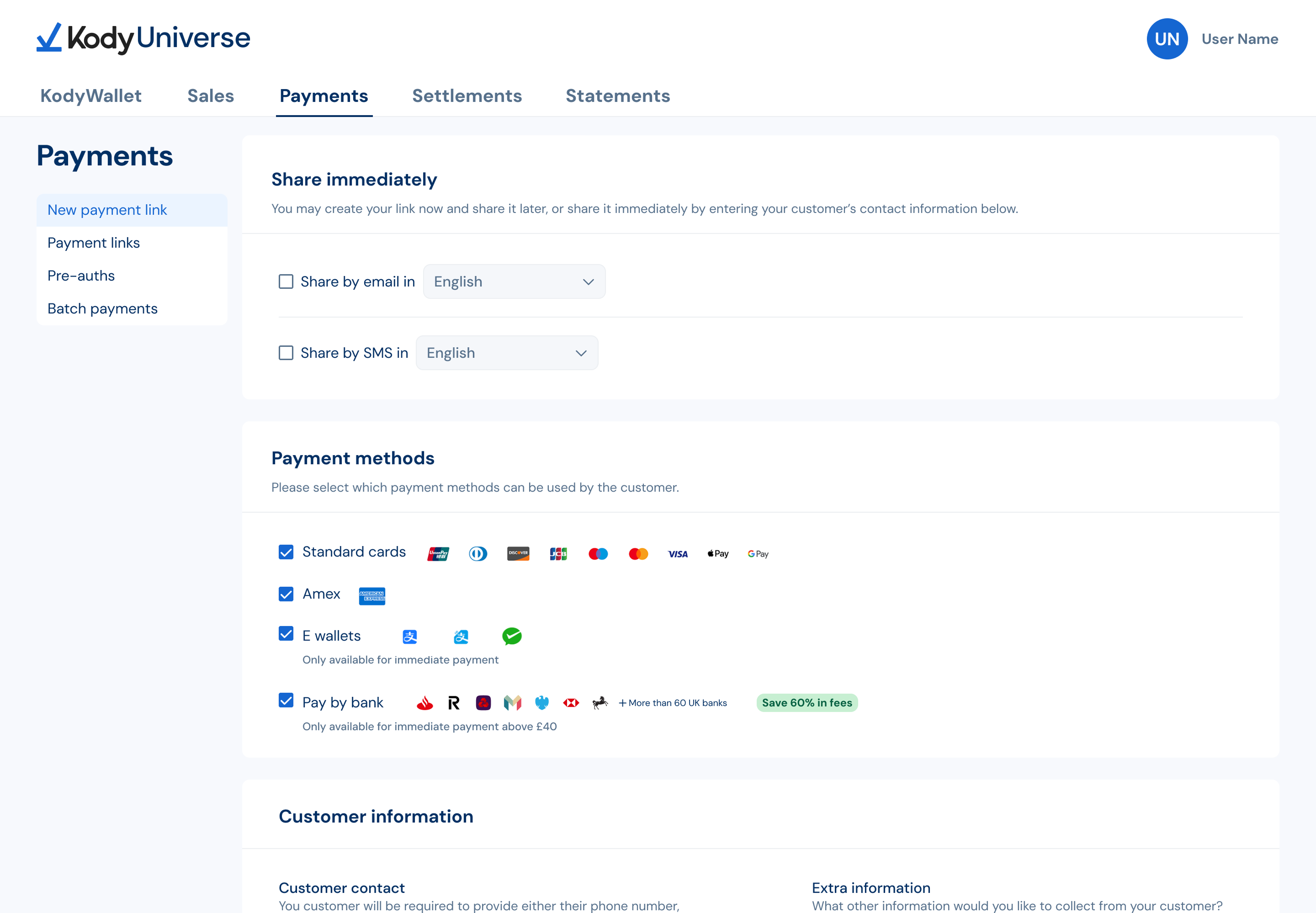

Choosing the Right Channel to Grow Pay by Bank

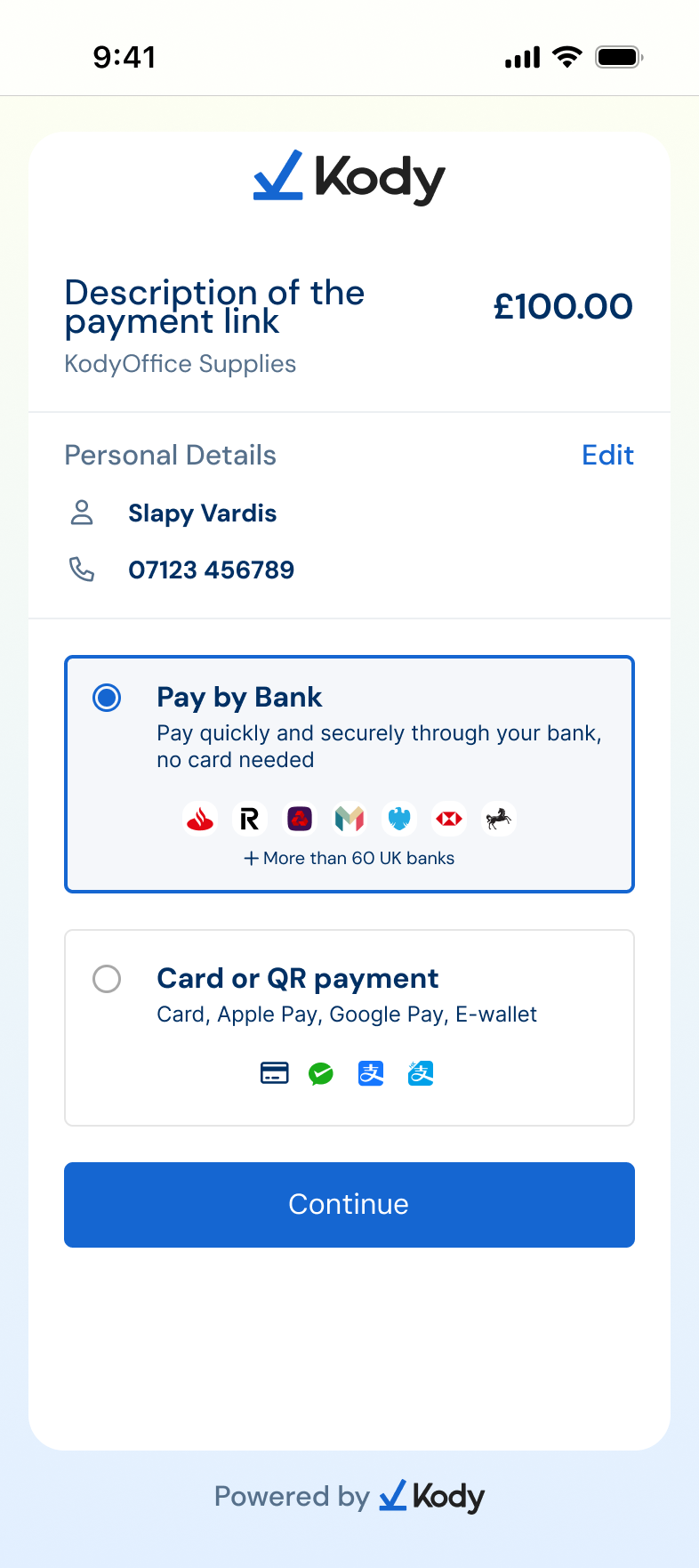

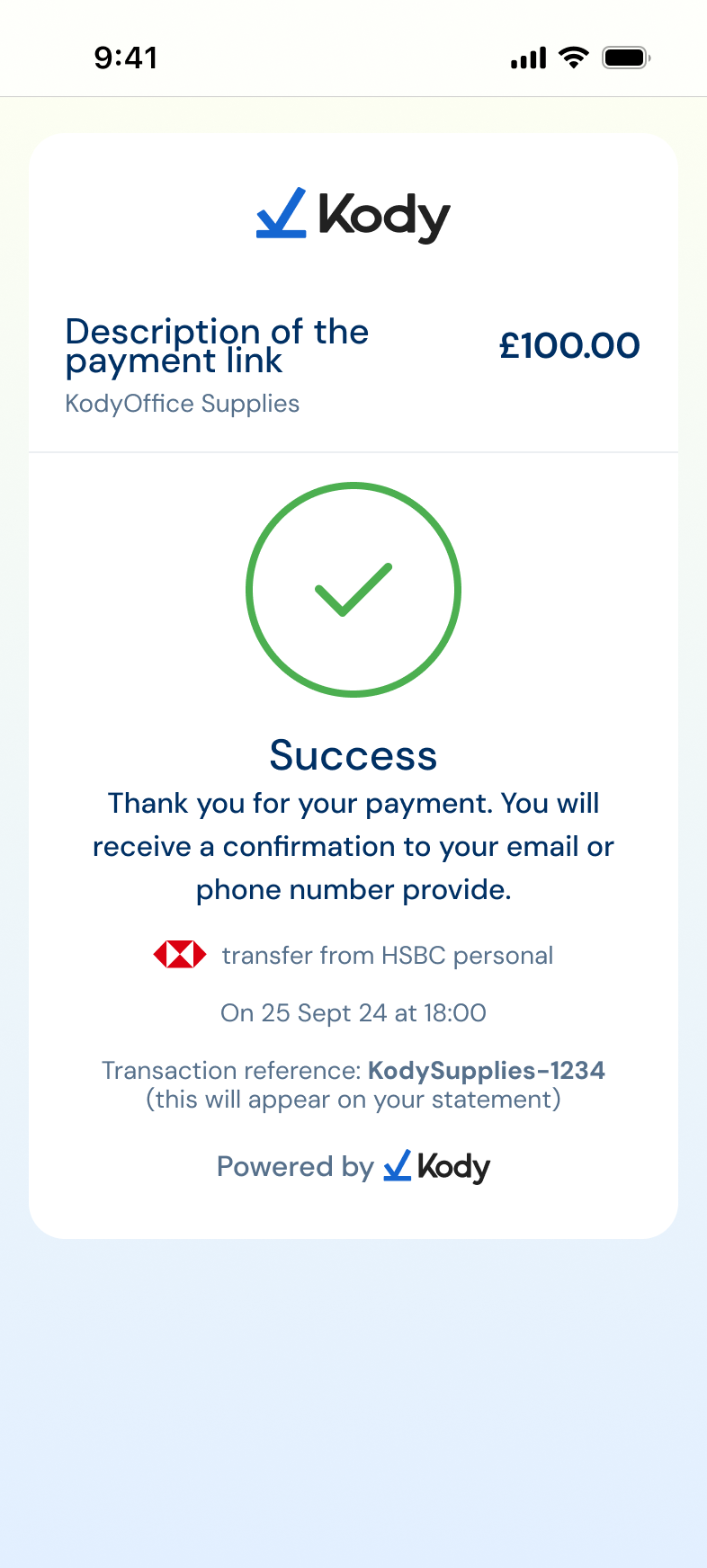

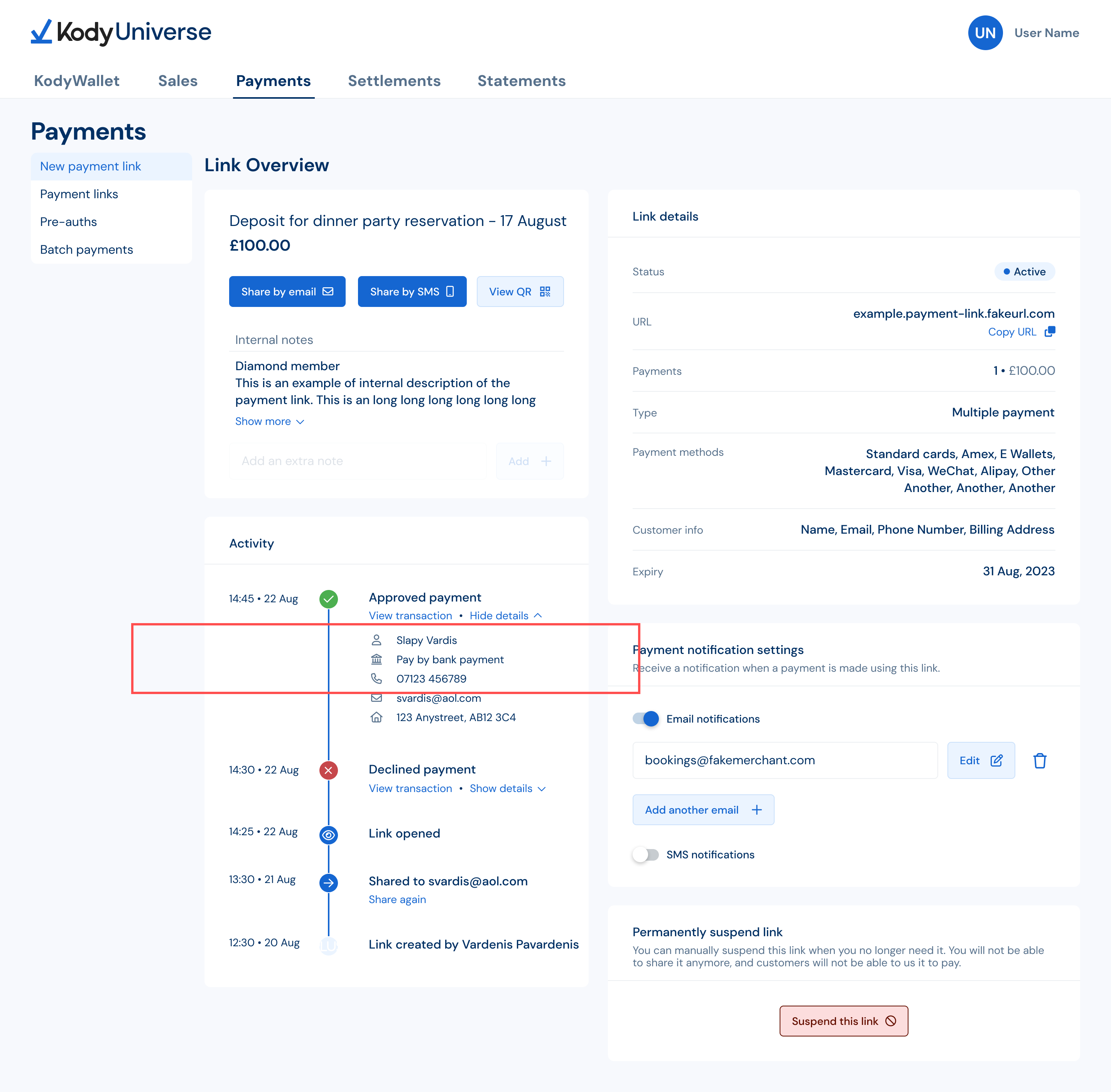

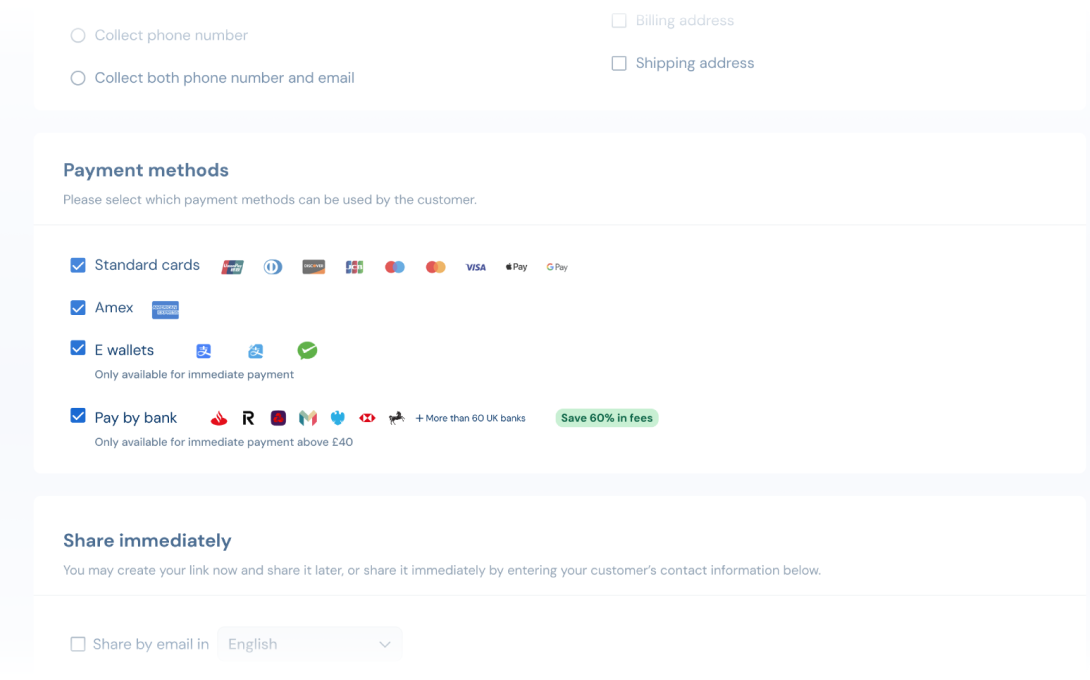

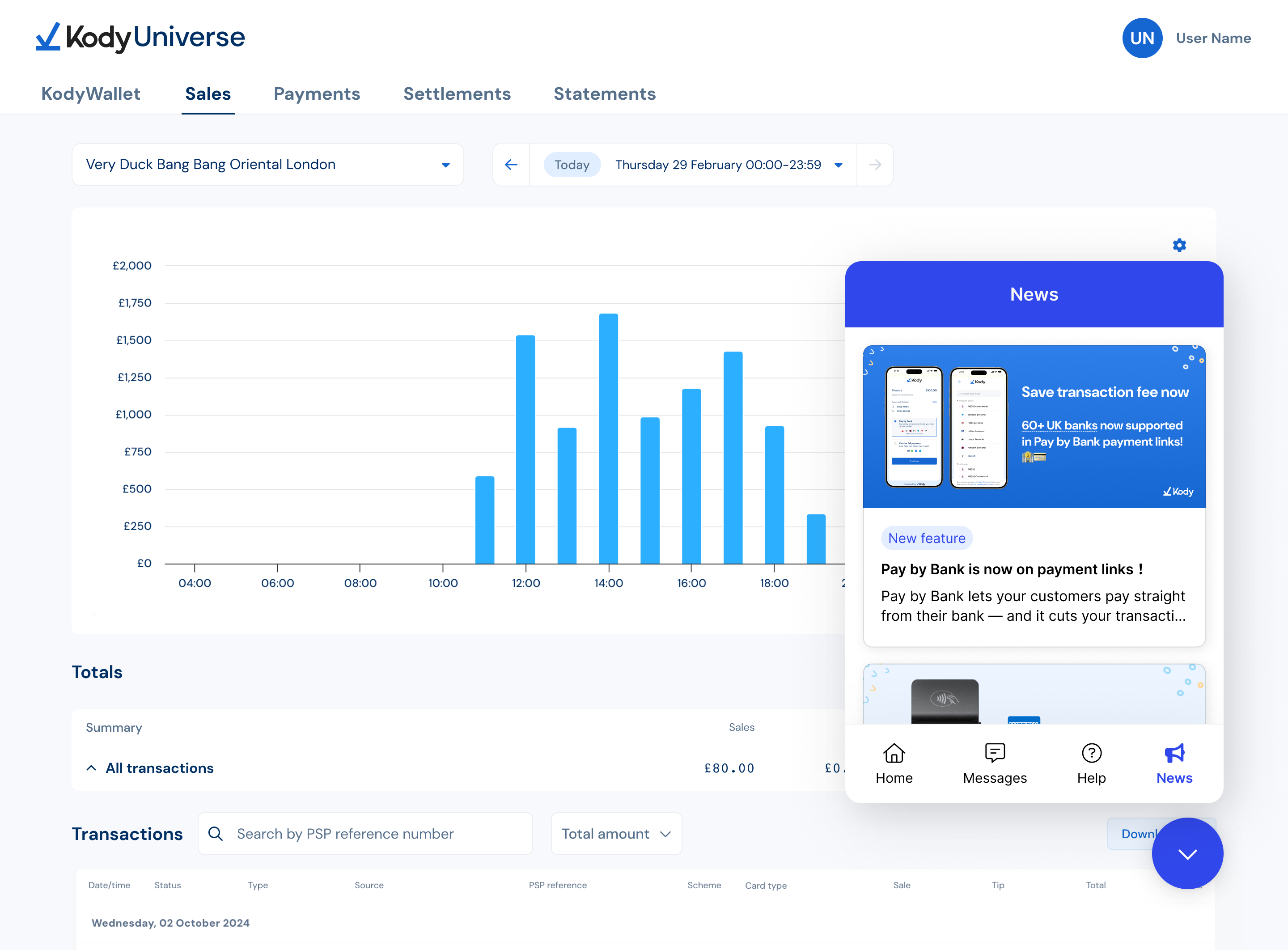

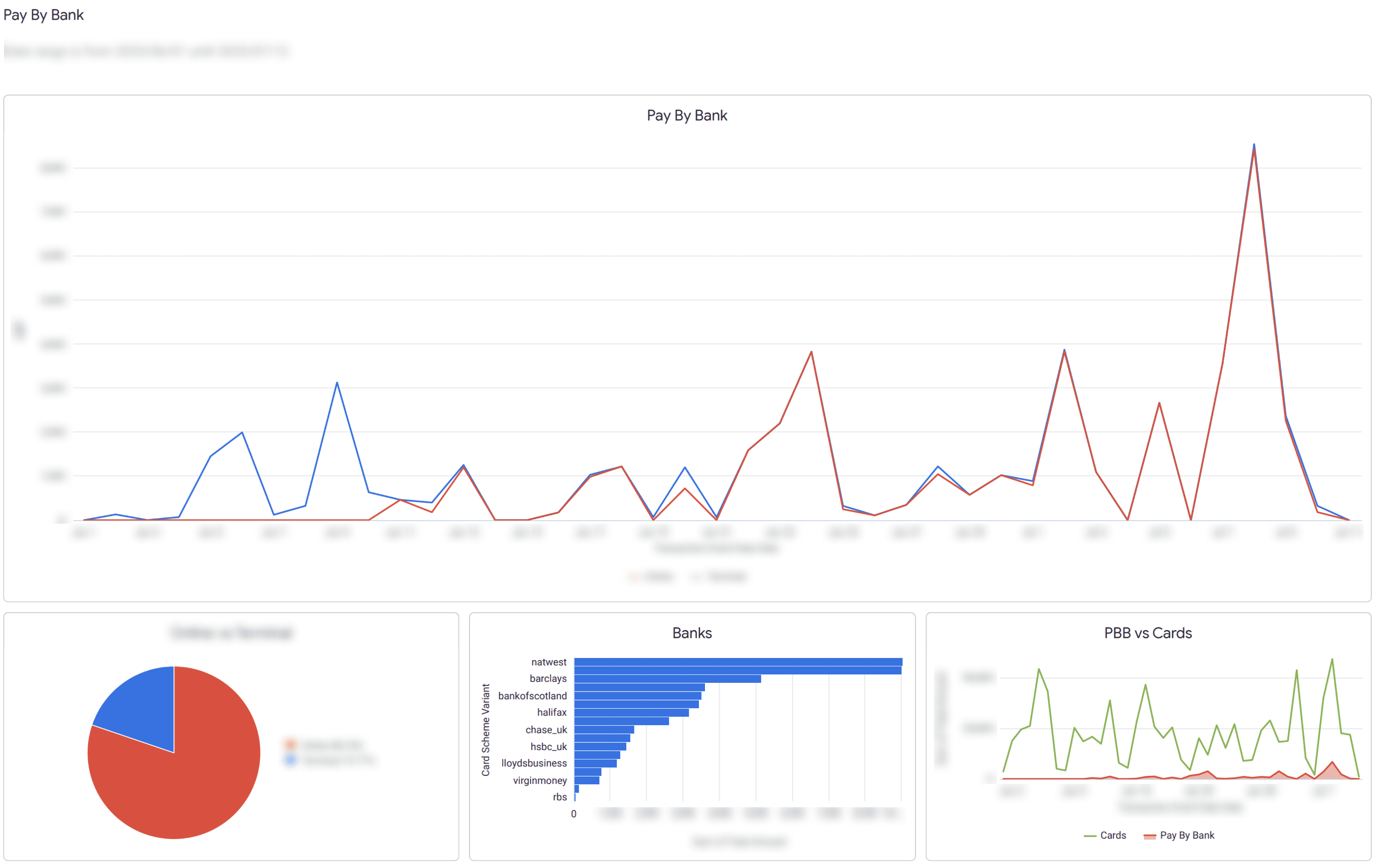

Two users defaulted away from Pay by Bank for different reasons. Merchants did not know it cut transaction fees by around 60%. Payers reached for card or Apple Pay out of habit, without considering it.

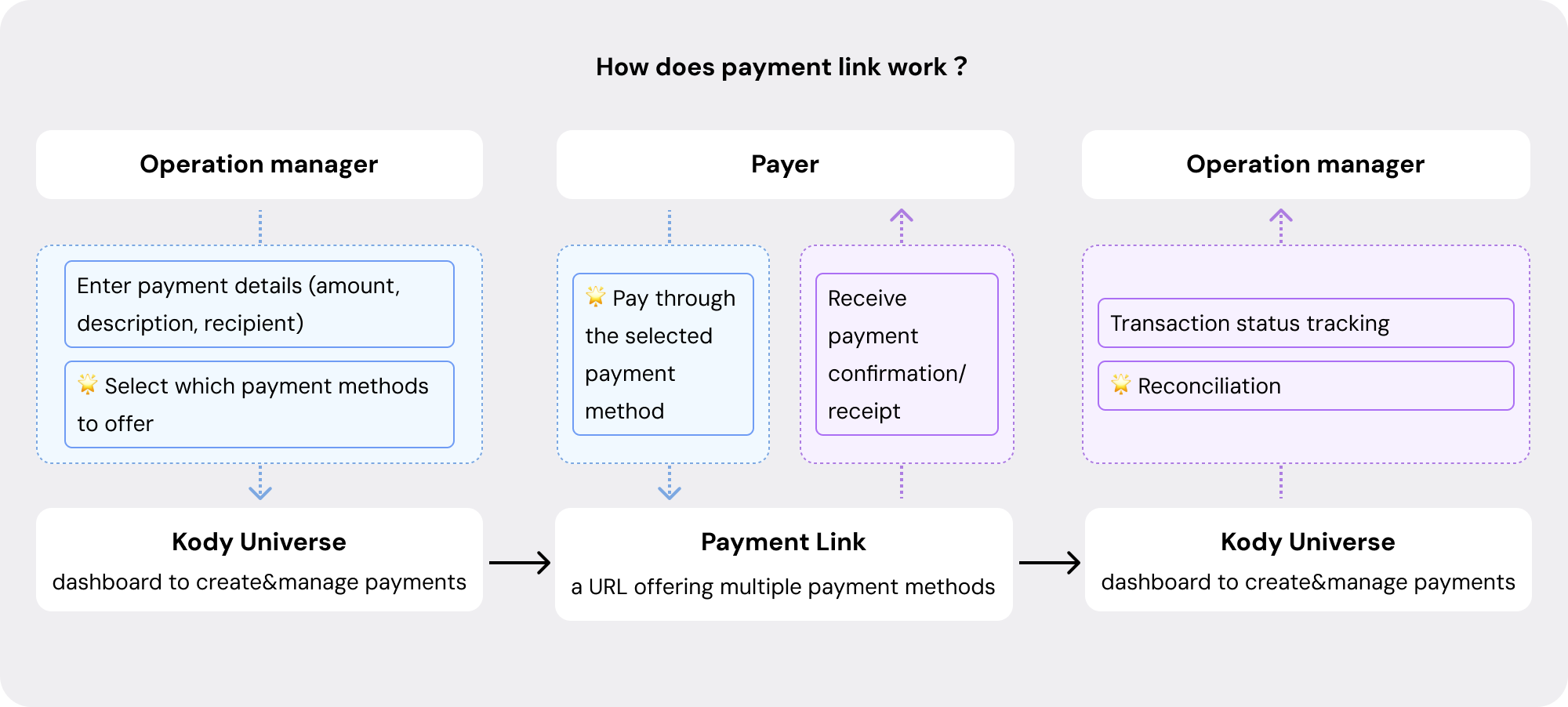

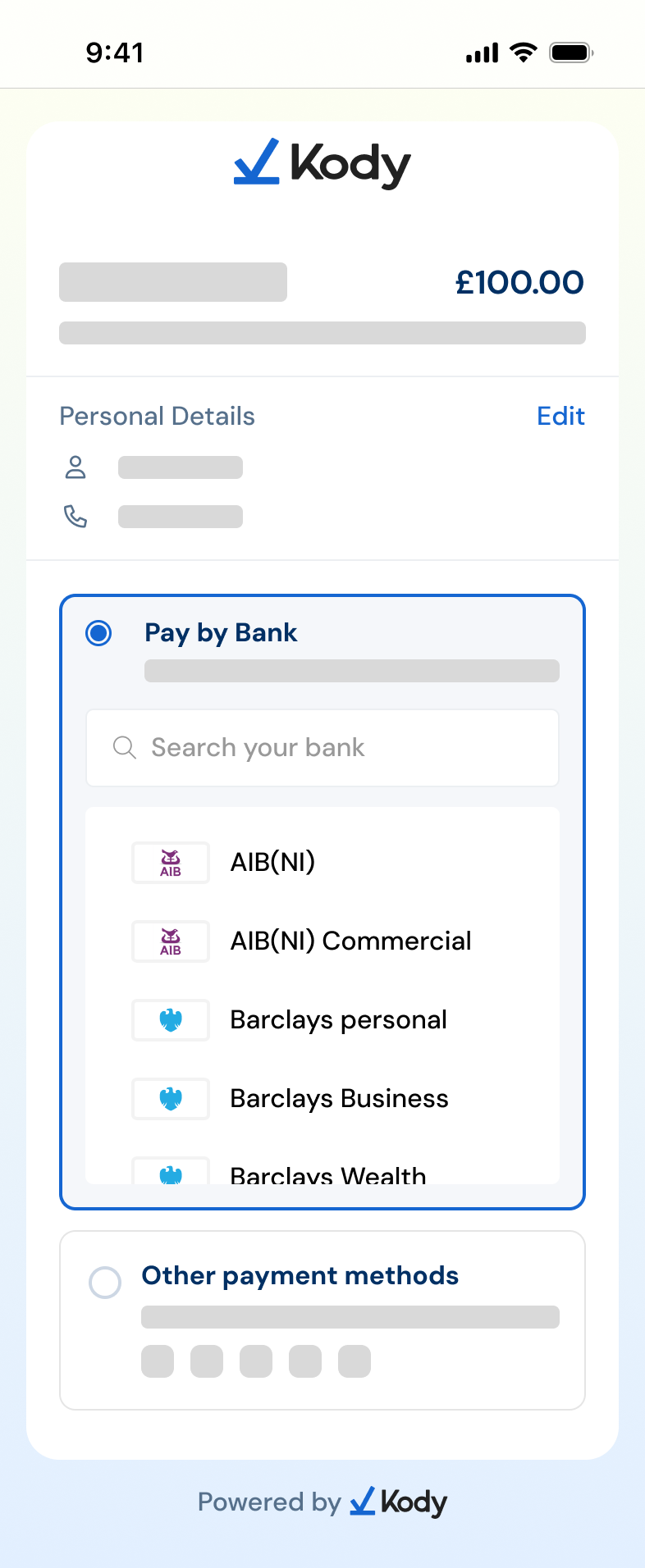

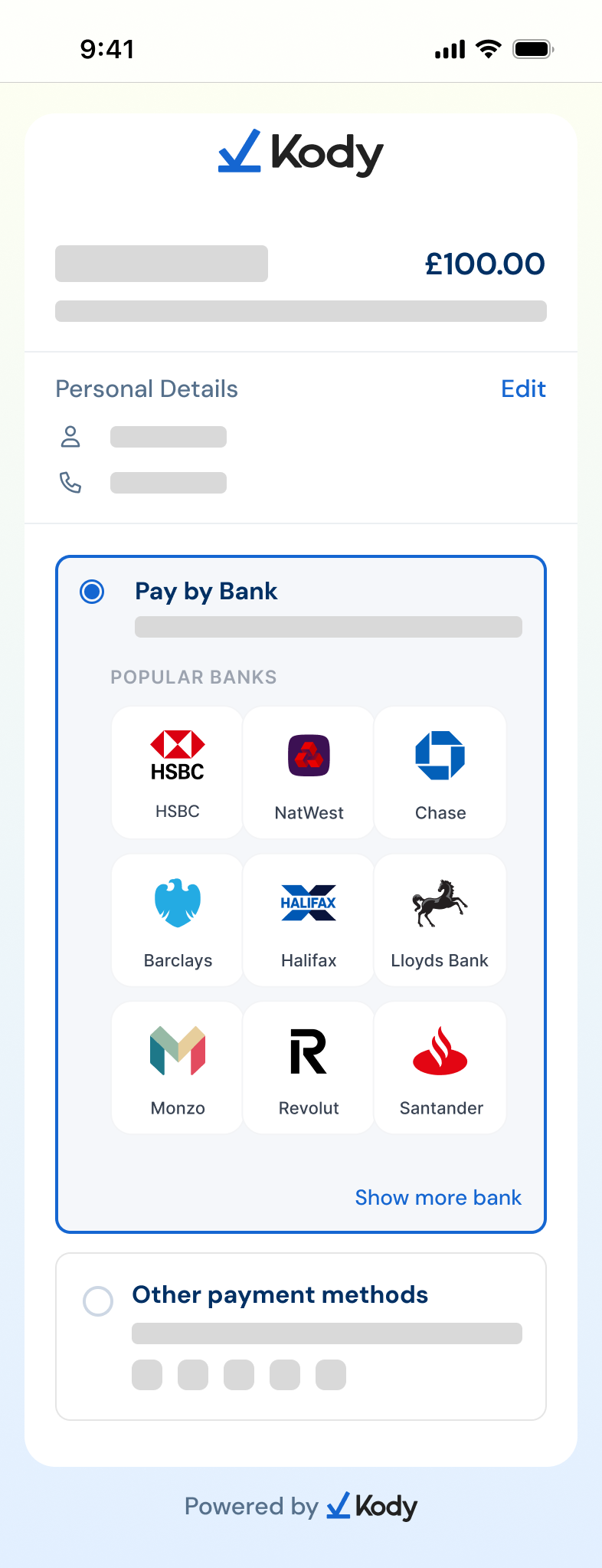

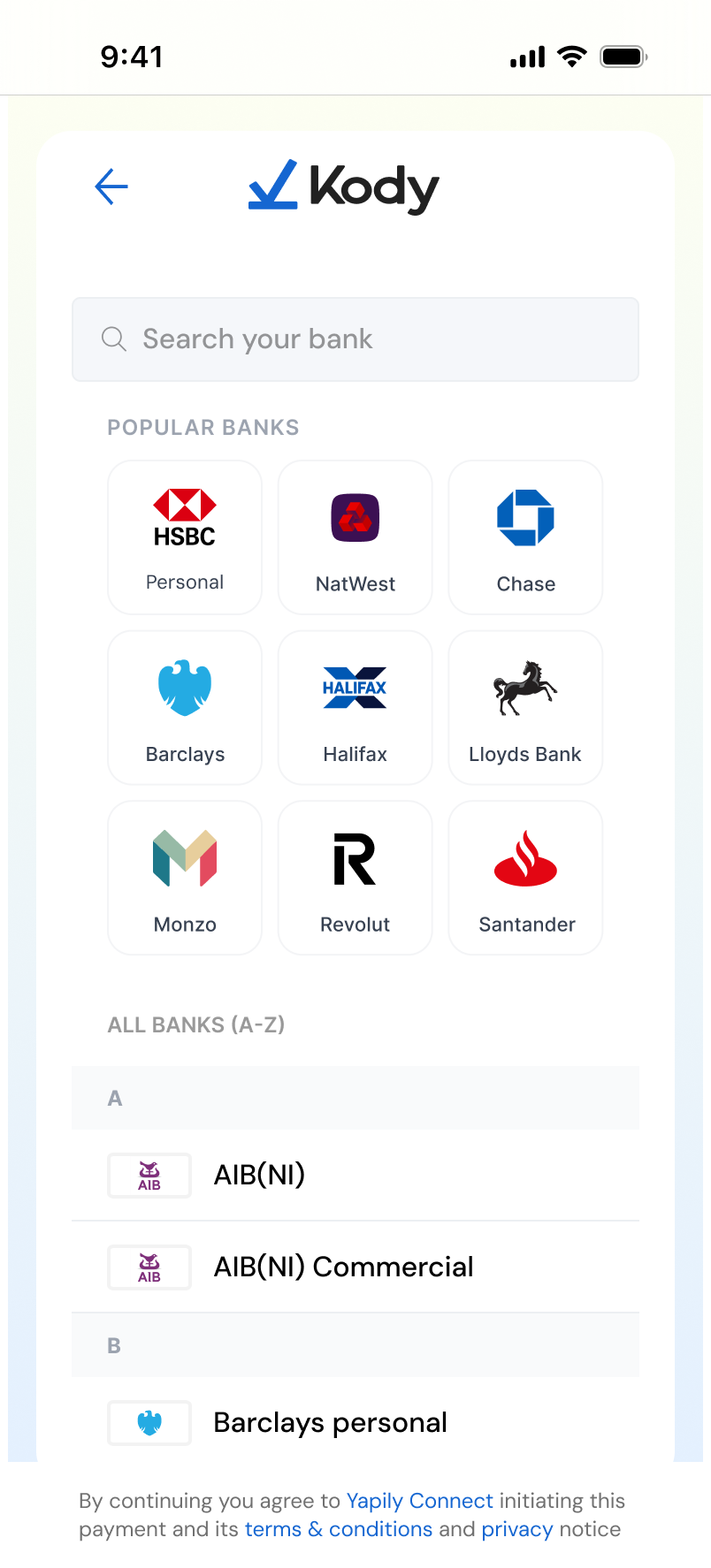

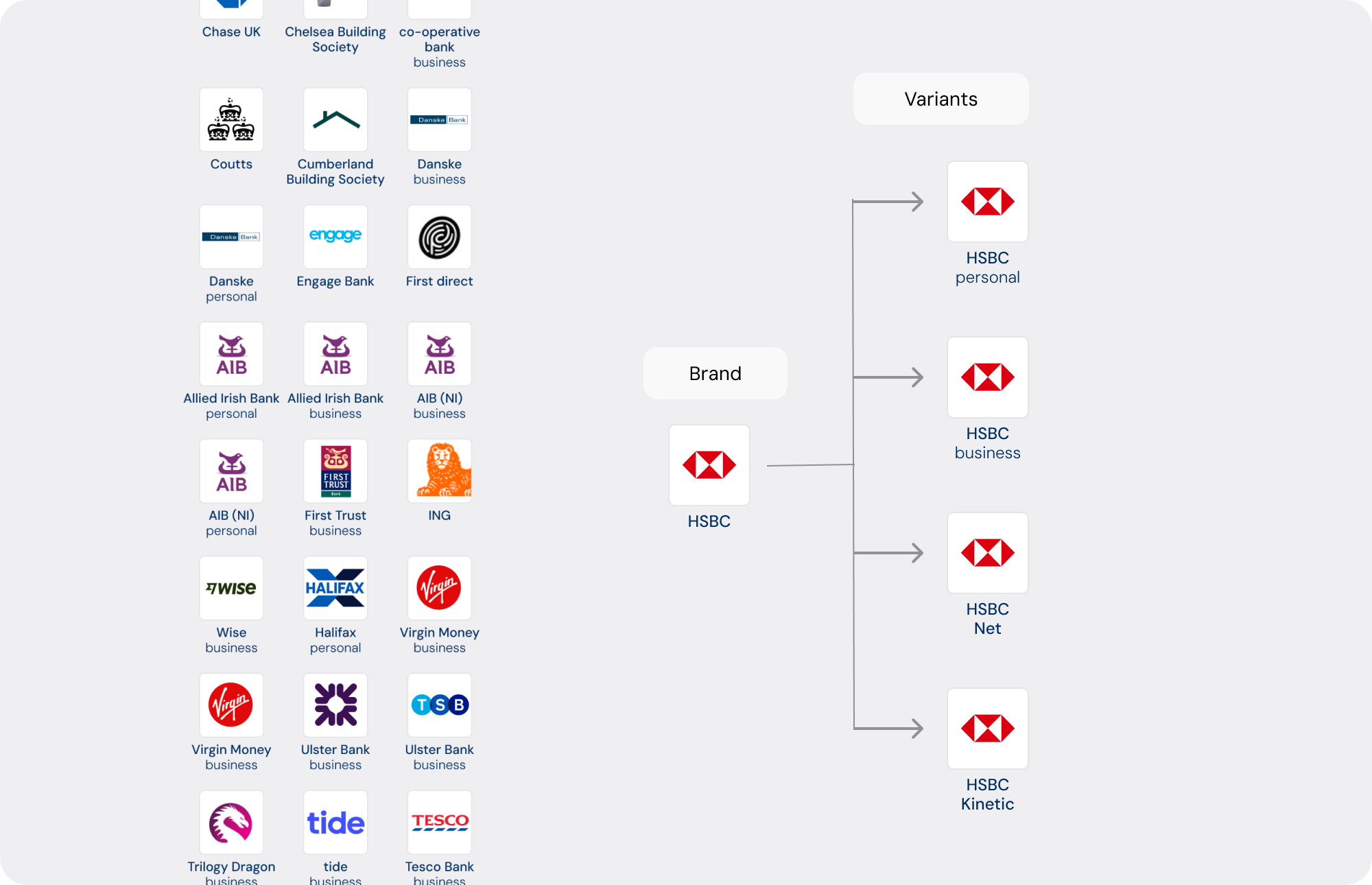

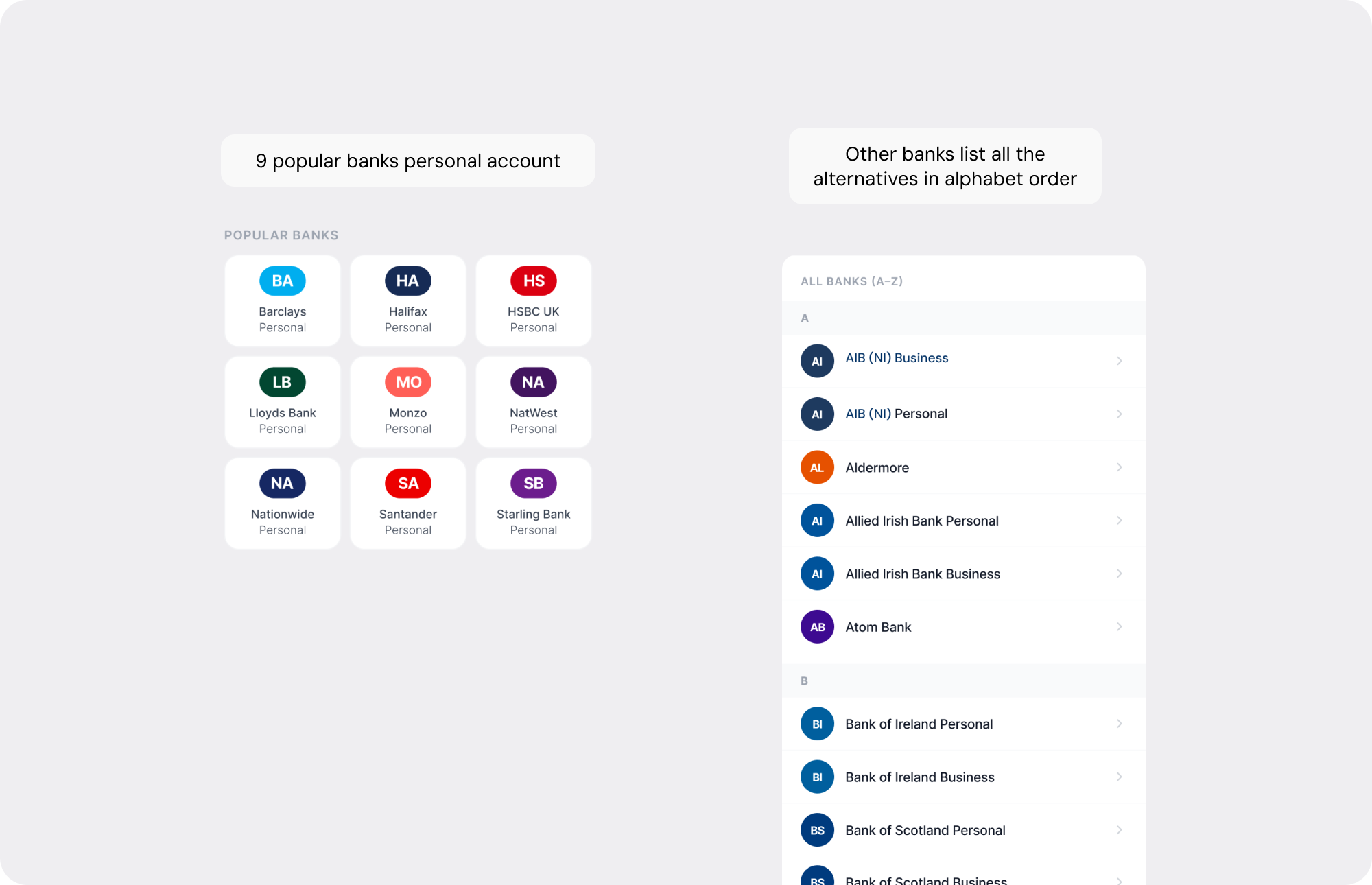

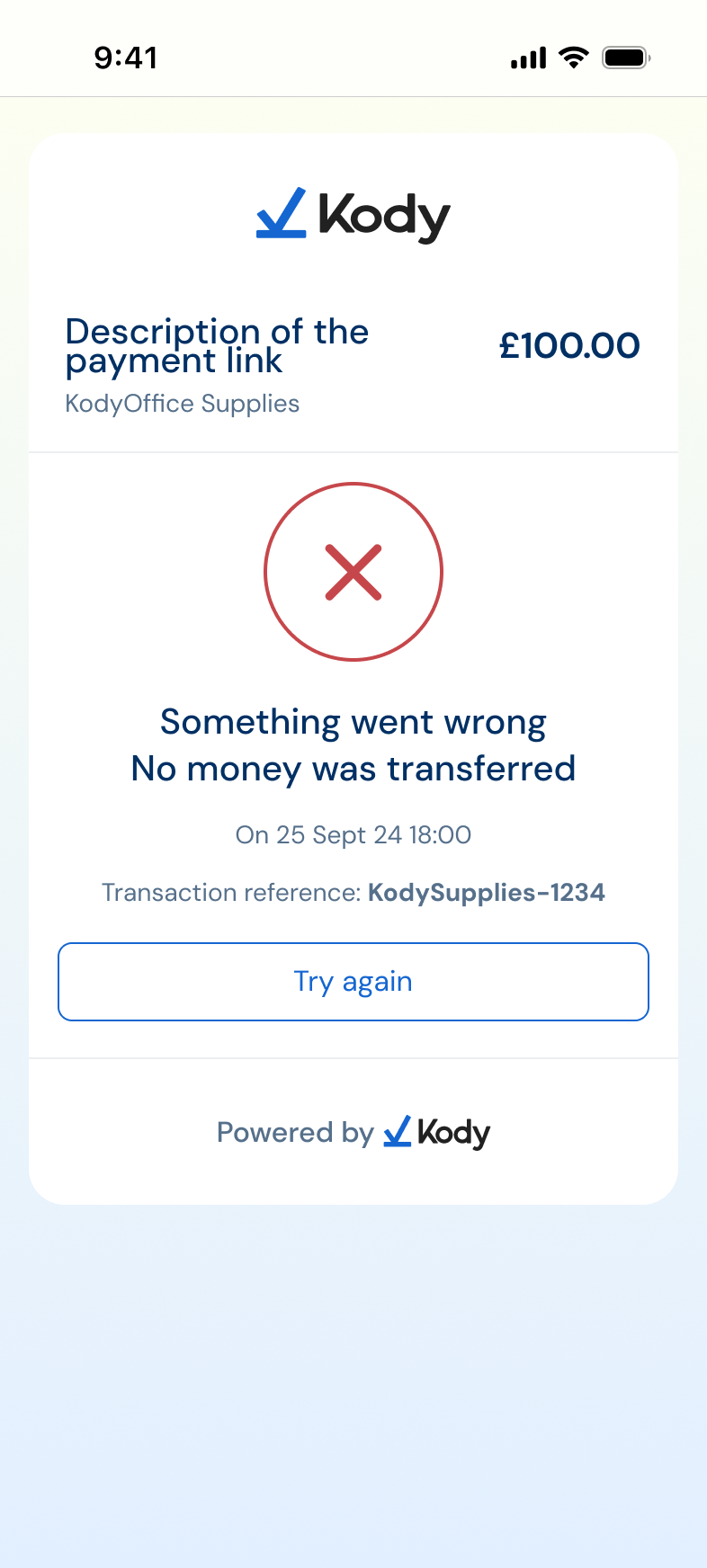

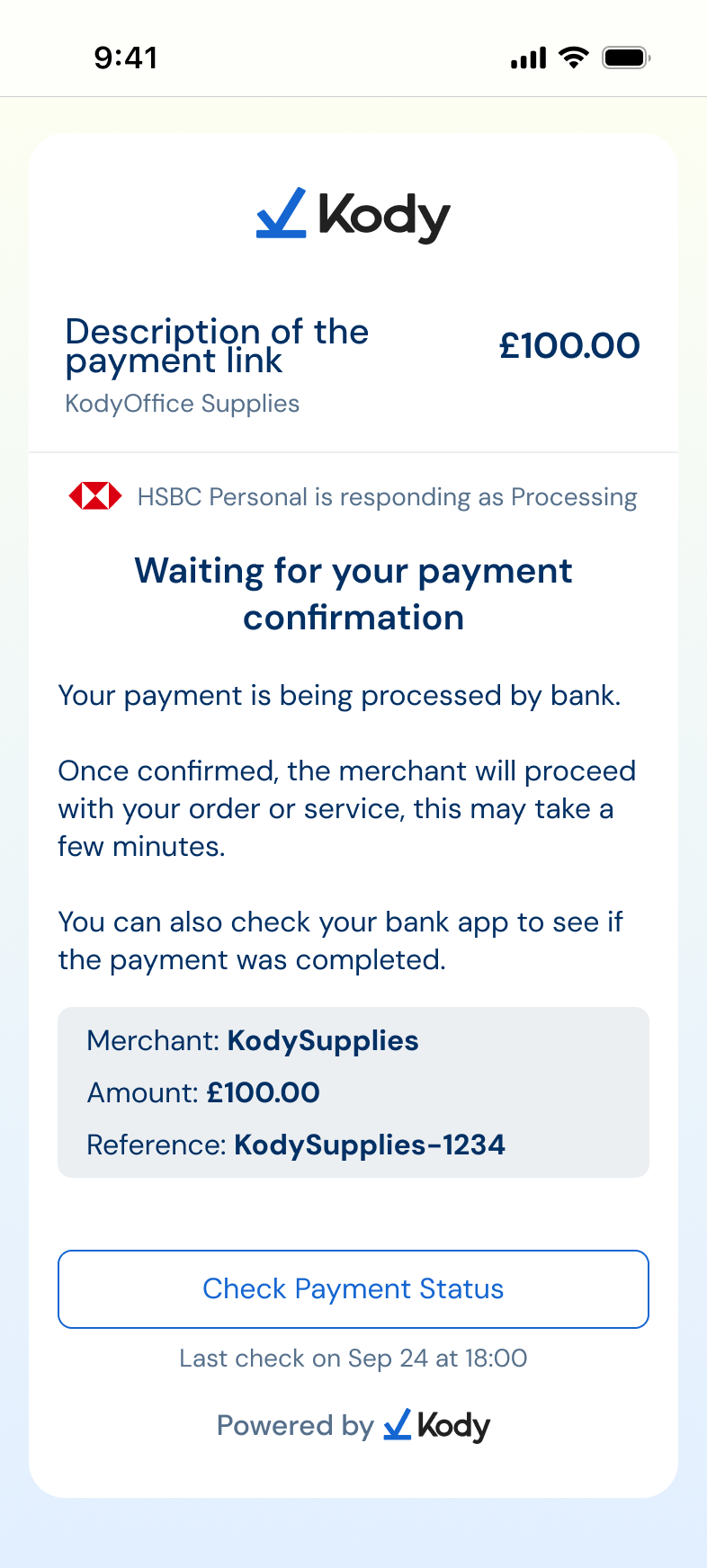

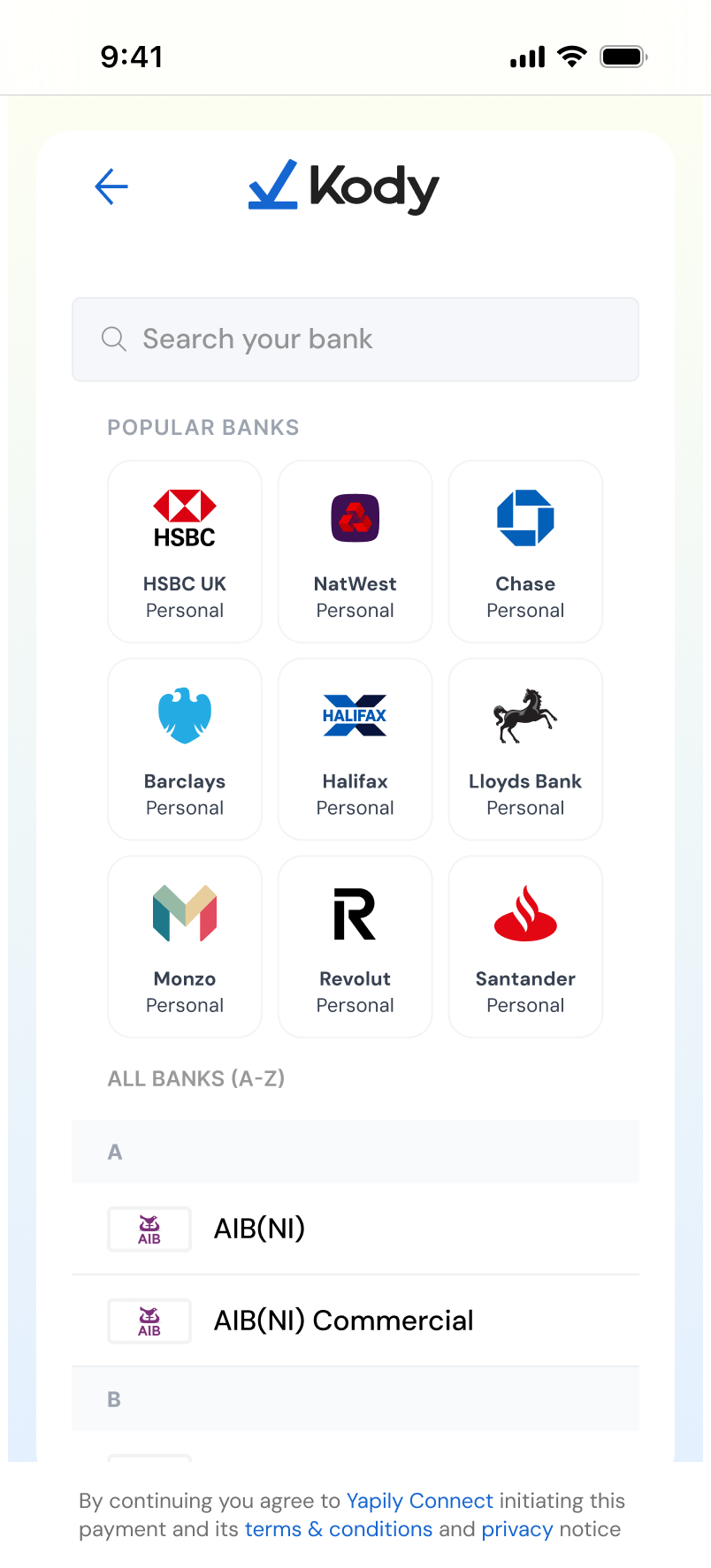

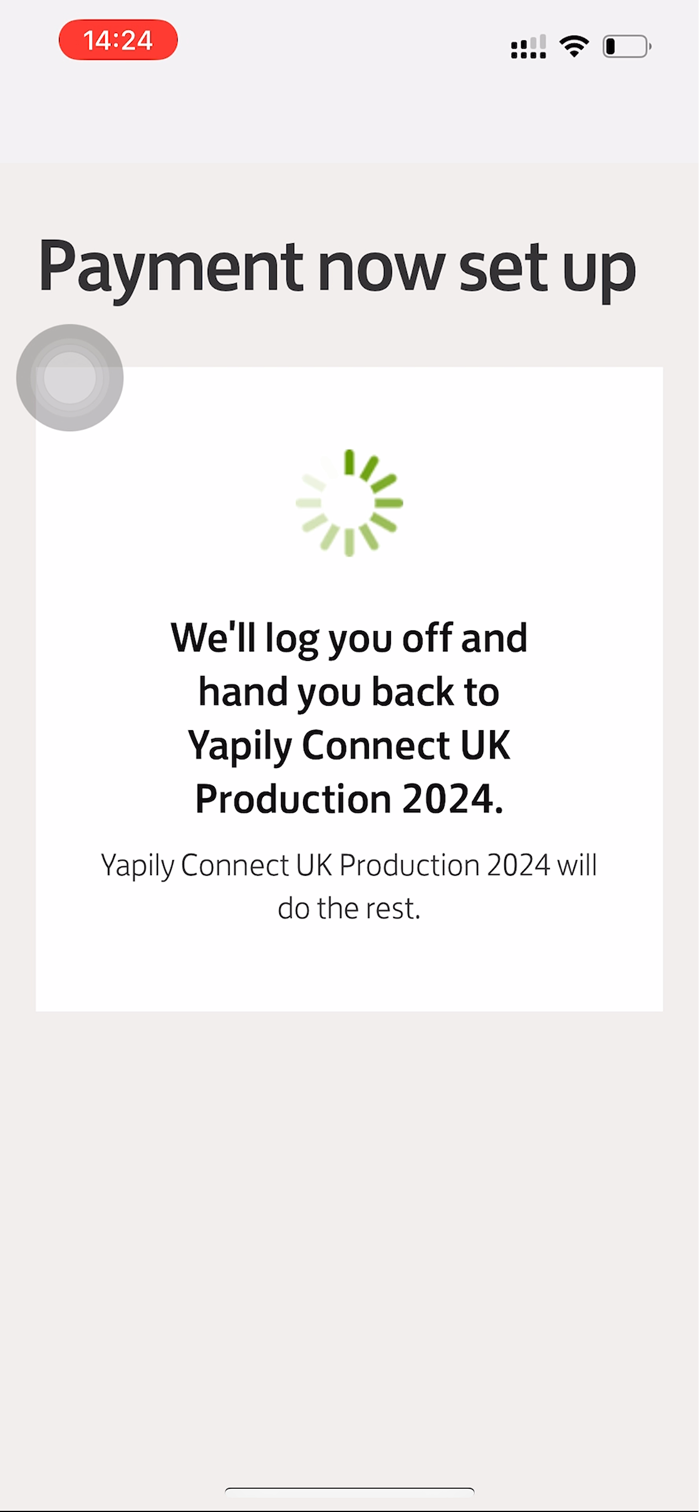

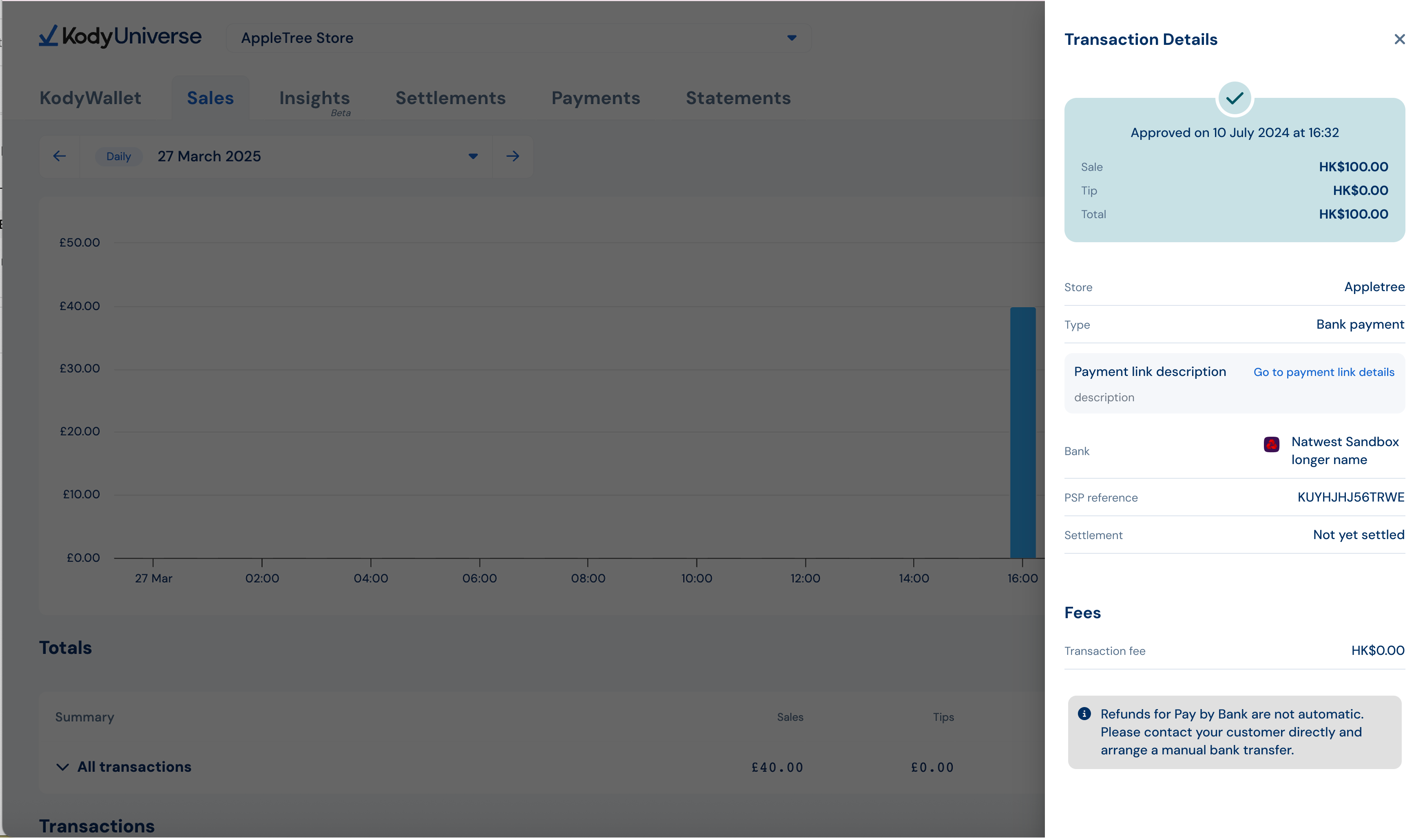

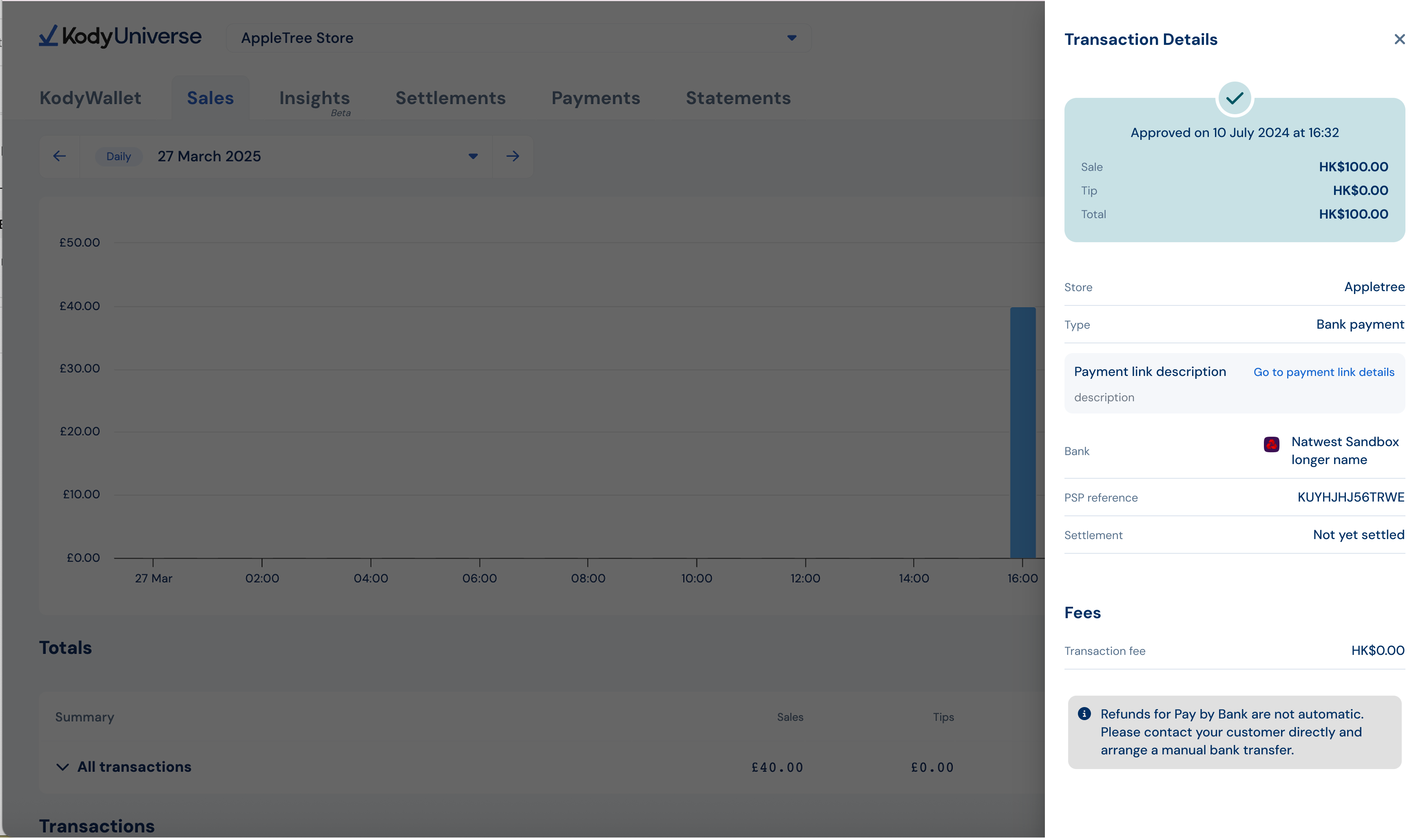

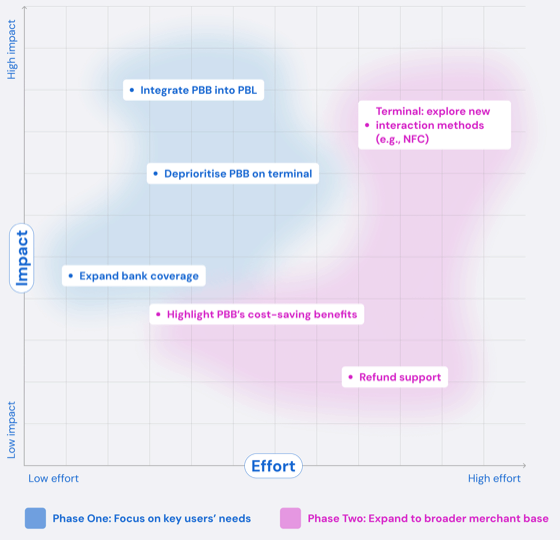

I designed for both: surfacing the fee saving to merchants at the point of link creation, and shaping how Pay by Bank is presented and selected in the payer checkout, including a bank selection flow built around our Open Banking provider's constraints.