Kody · 2025 · B2B2C · Open Banking

Choosing the Right Channel to Grow Pay by Bank

Detailed process of how I contributed to finding the strategy and pivoting to the correct channel for Pay by Bank

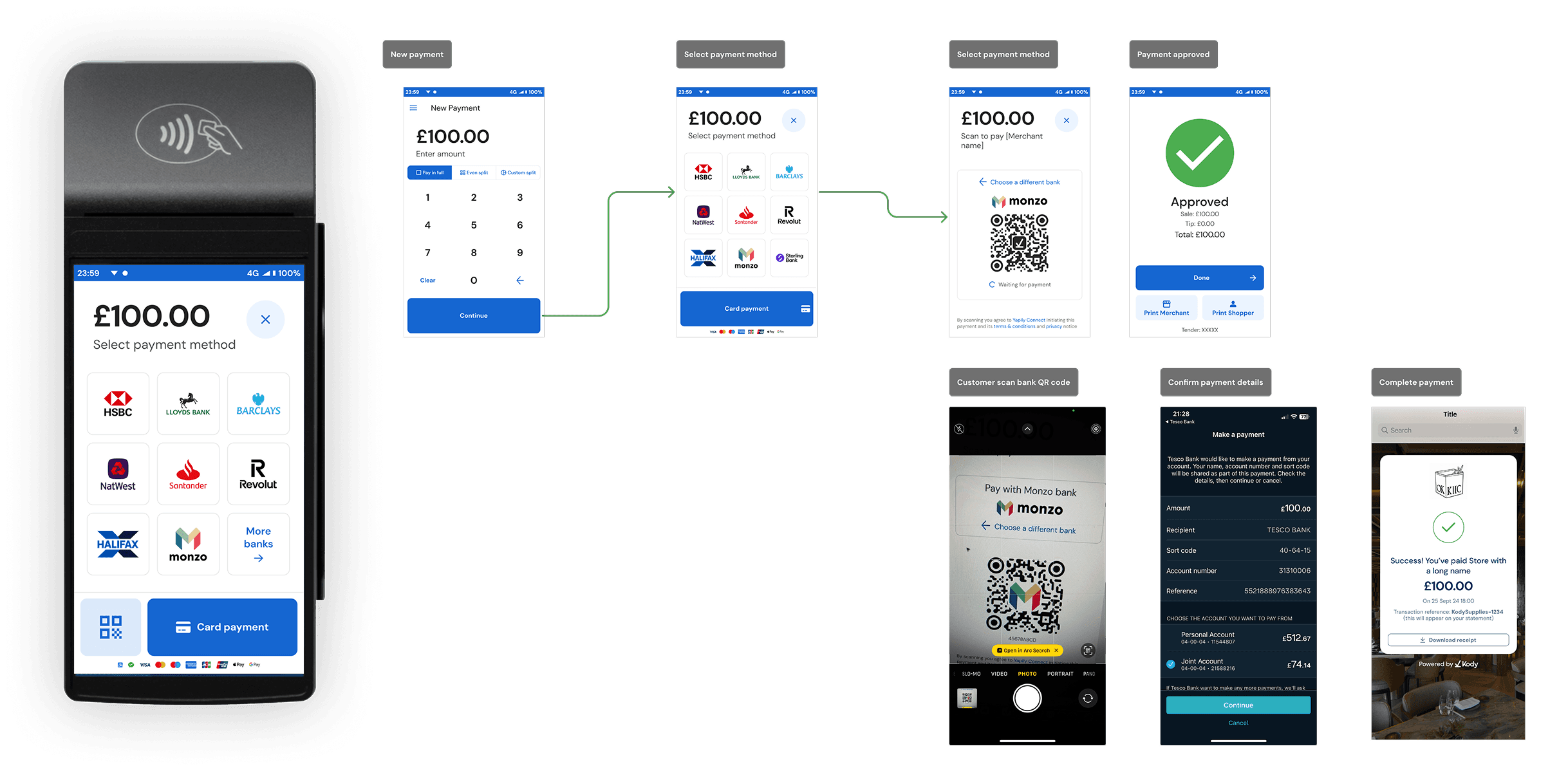

At Kody, a UK payments startup, leadership asked the team to add 64 more banks to our in-person terminal in order to lift Pay by Bank adoption. After one week of user research, I made the case for a different direction: Pay by Bank is a context-sensitive product, and the terminal wasn't the right context. The team pivoted to integrating Pay by Bank into Pay by Link instead — a channel where the product's strengths actually translate into adoption.

After pivoting, Pay by Bank transaction volume grew 120% in the first month.

Case B

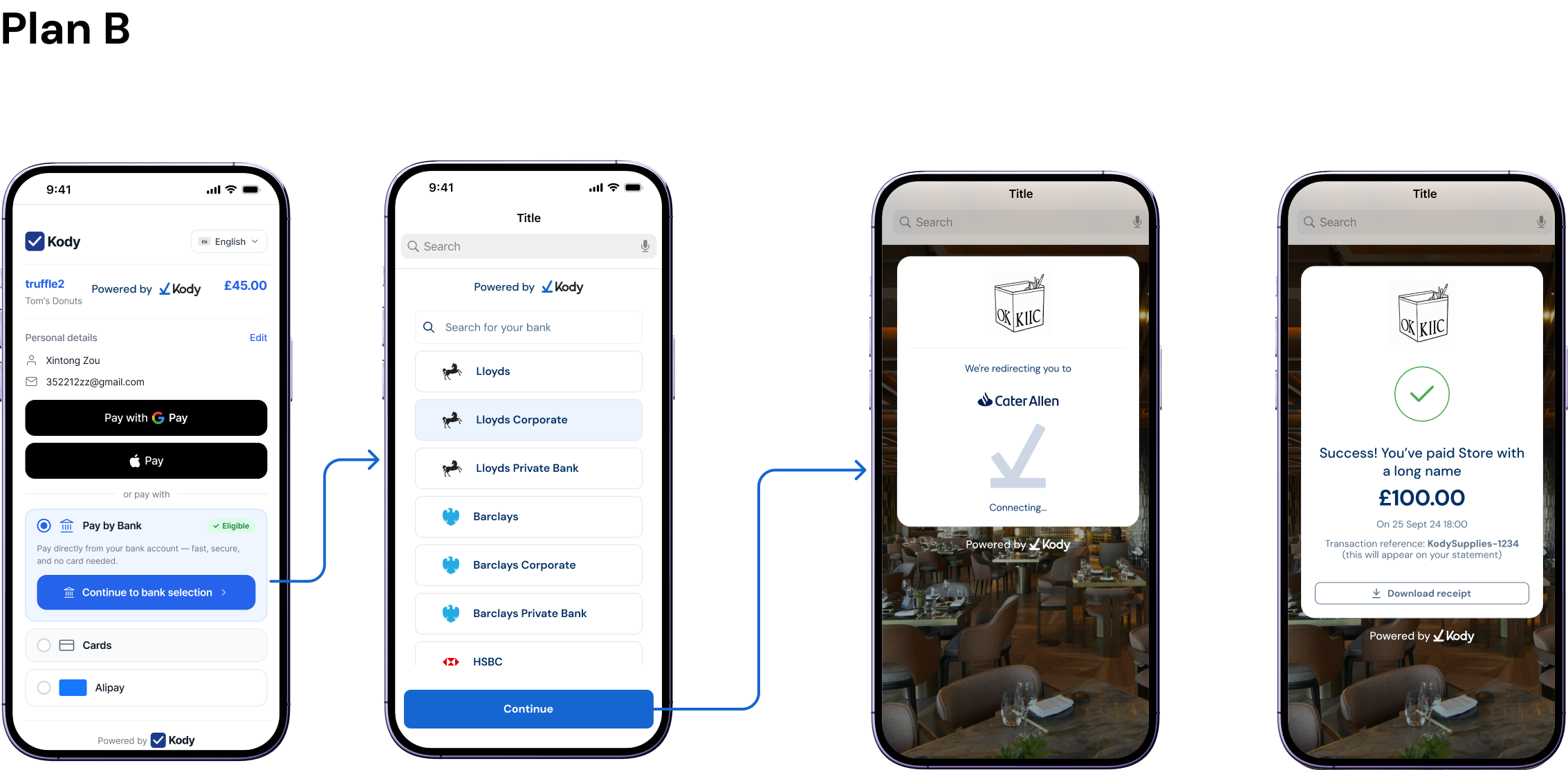

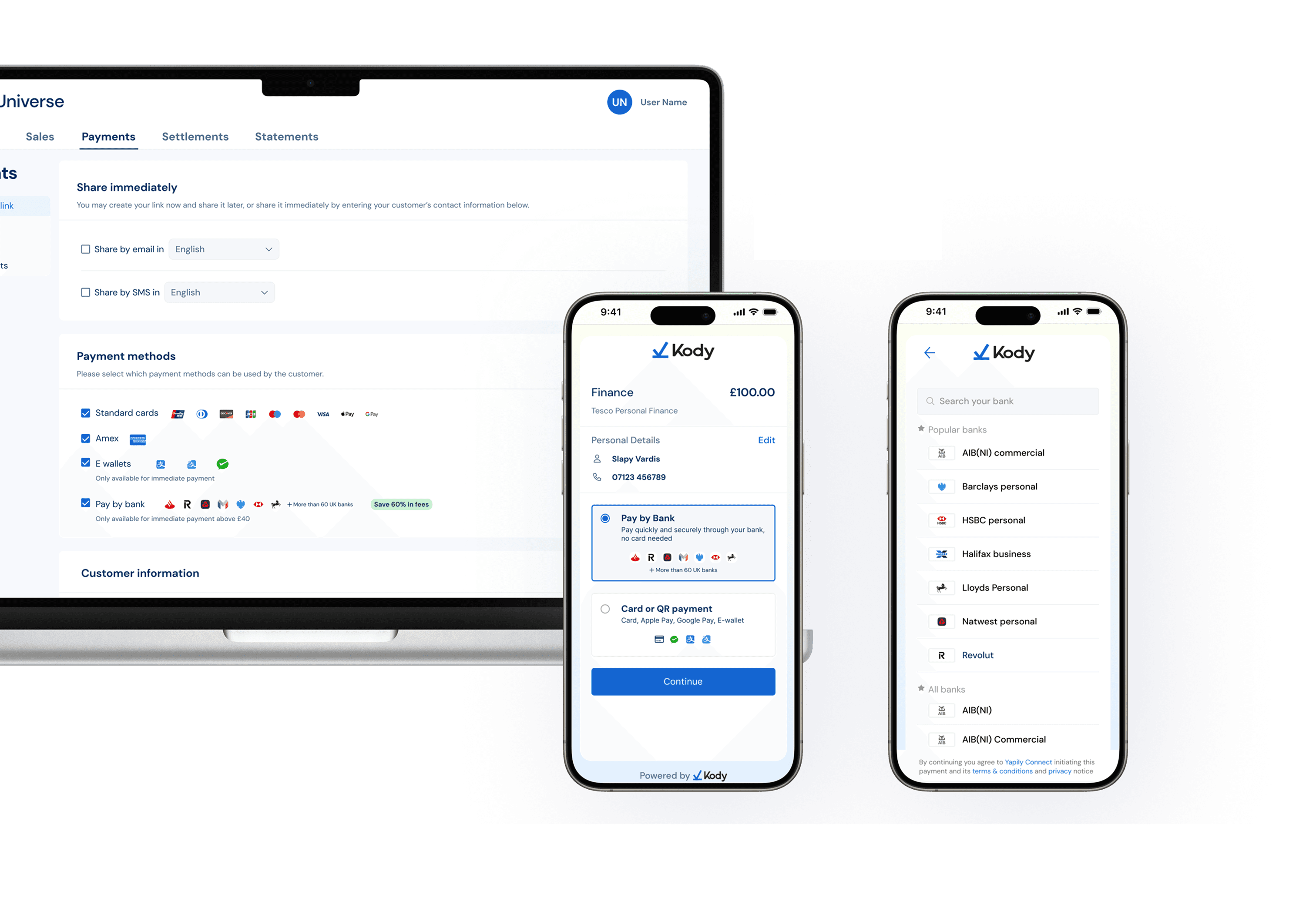

→Designing Pay by Bank for Pay by Link