Kody · 2025 · B2B2C · Open Banking

Choosing the Right Channel to Grow Pay by Bank

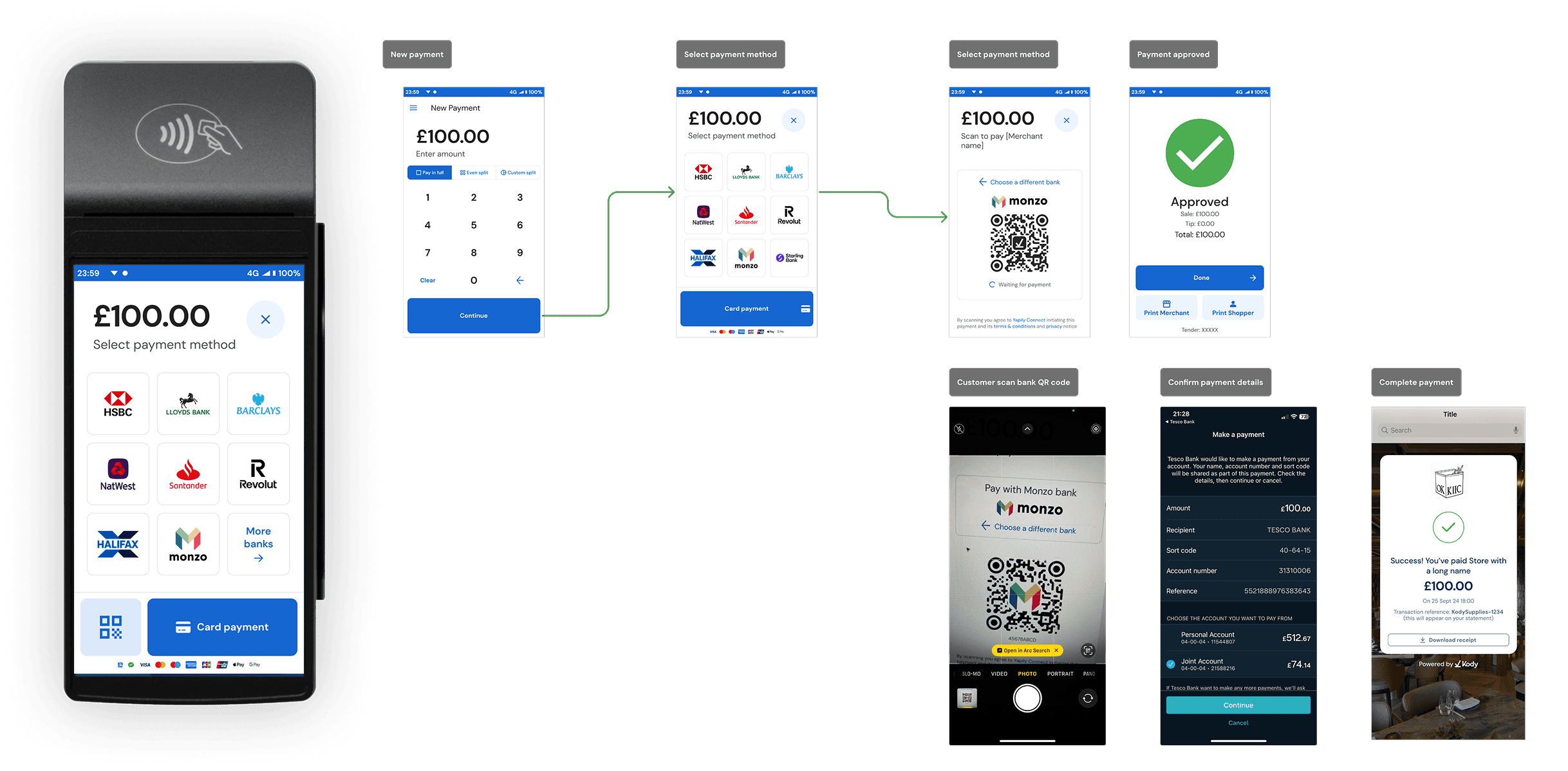

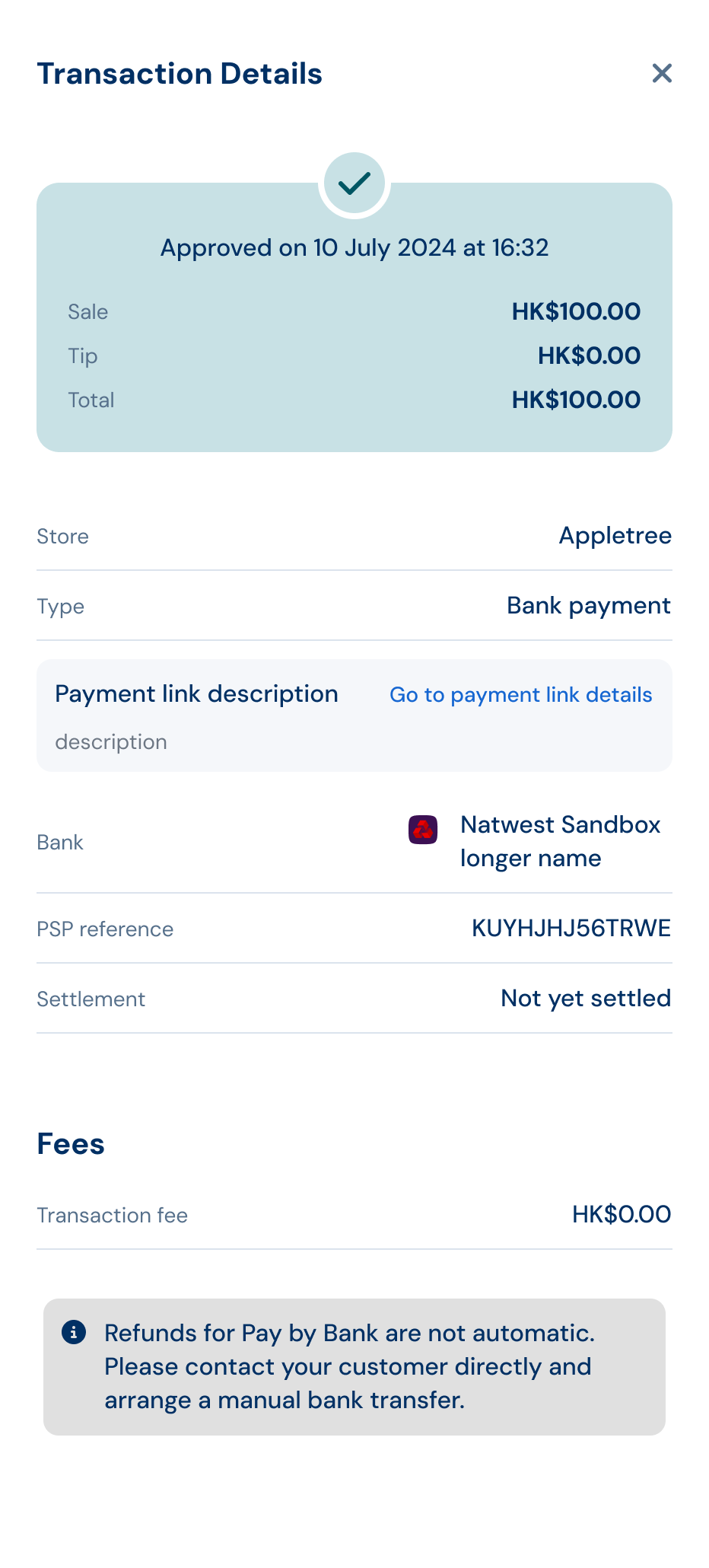

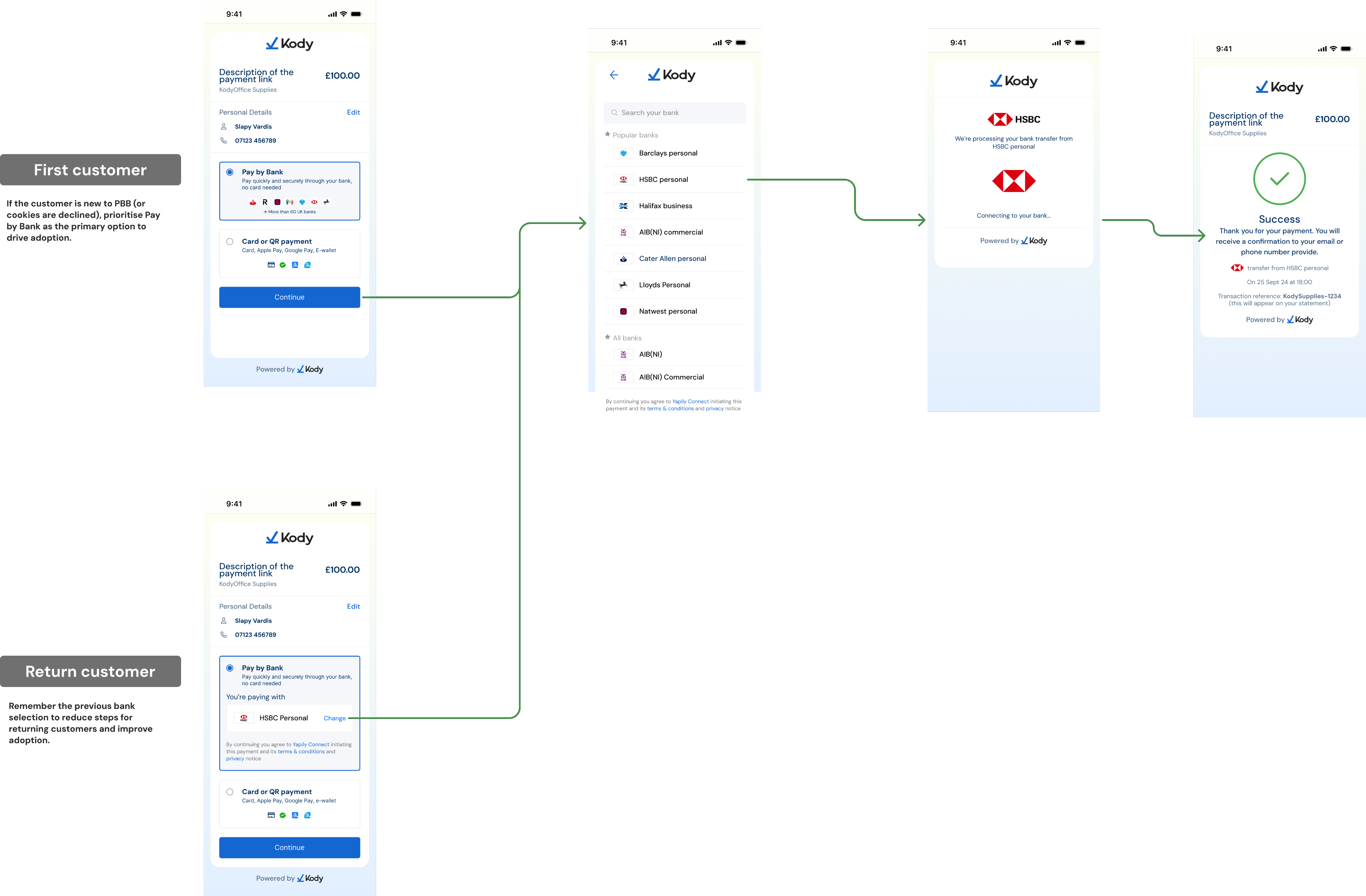

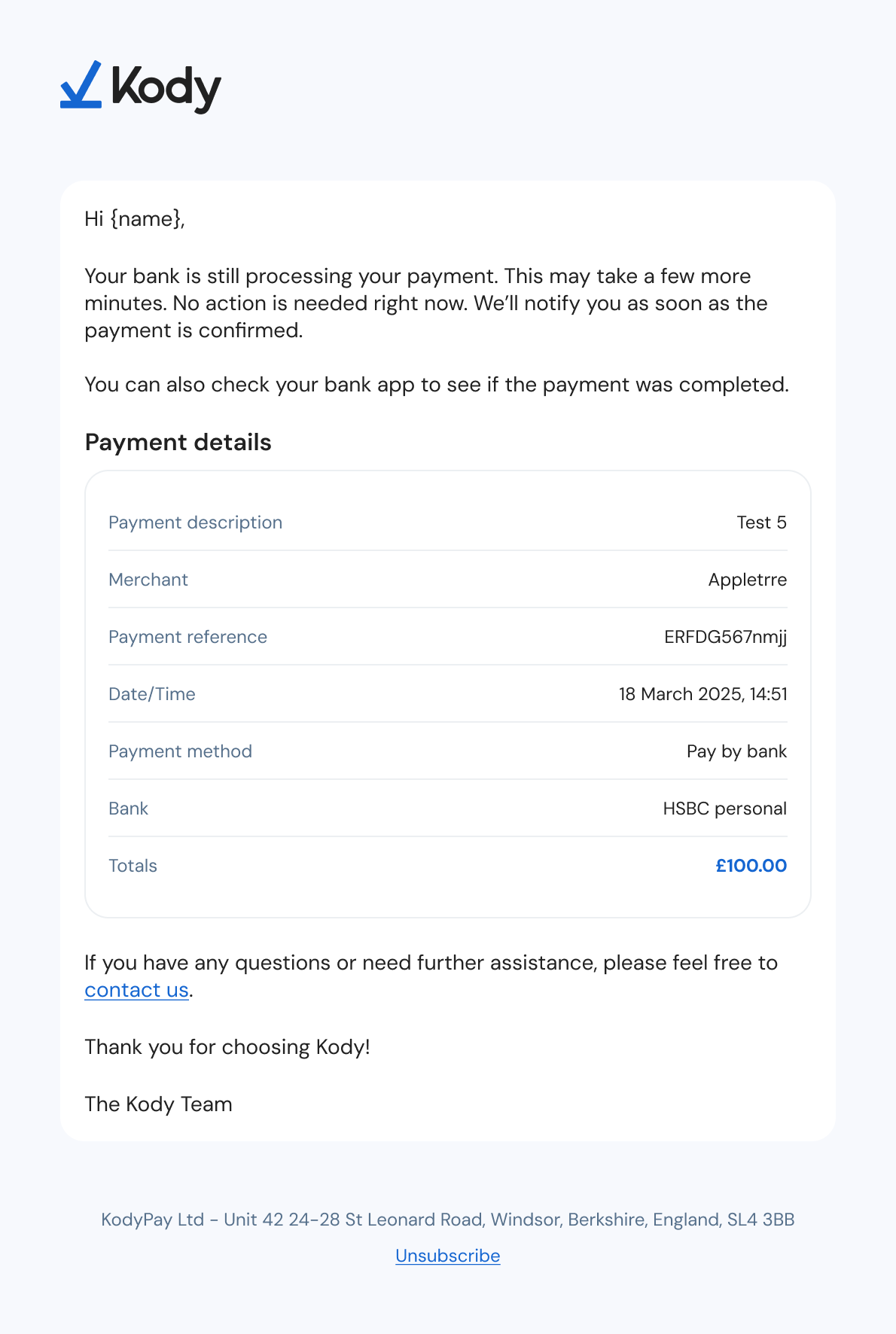

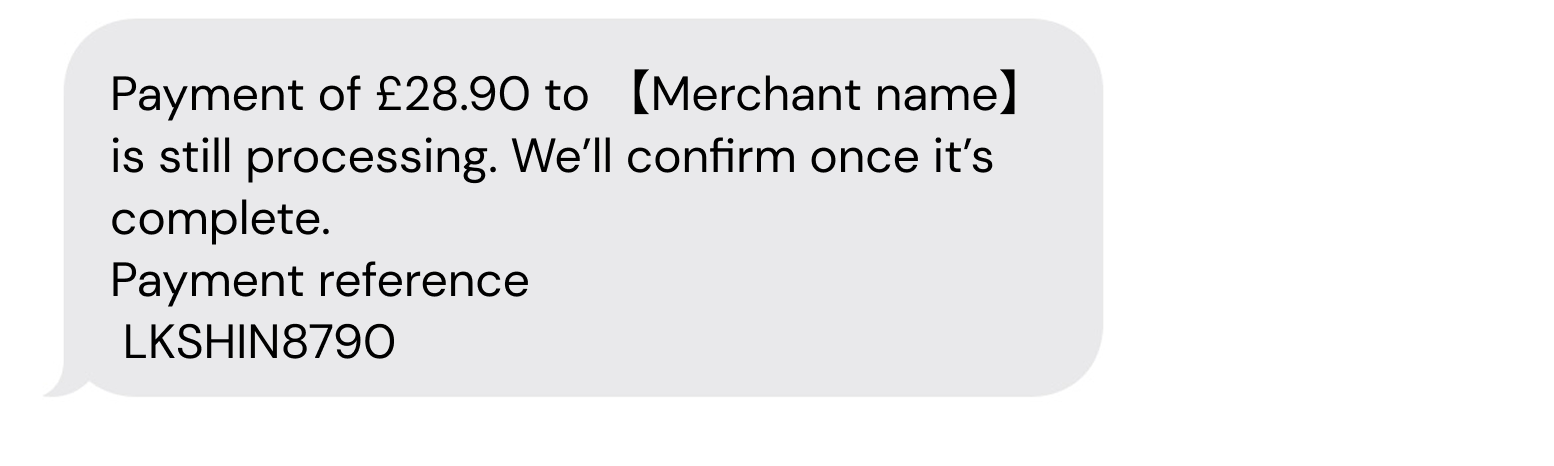

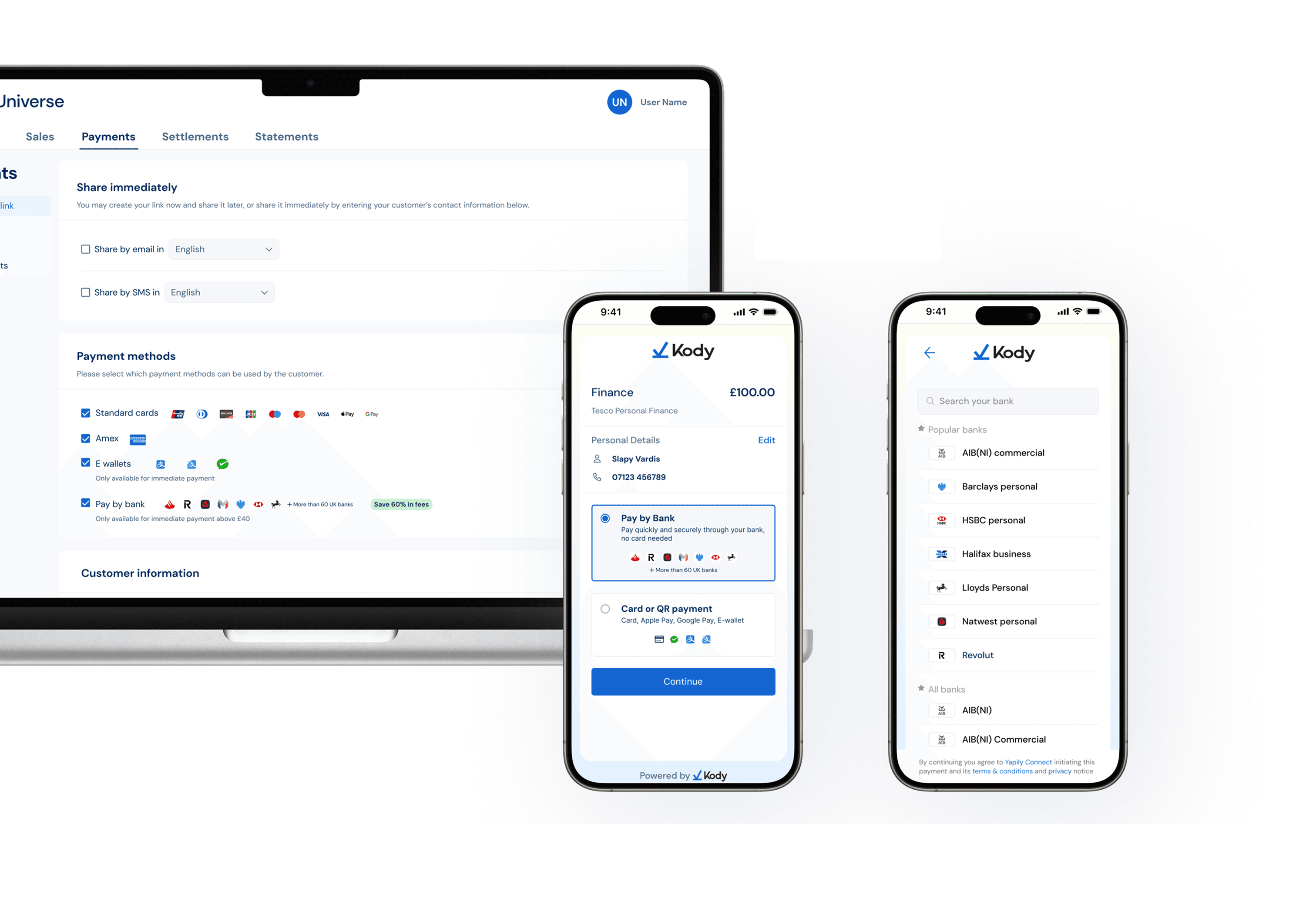

How pivoting Pay by Bank from POS terminals to payment links increased adoption by 120%

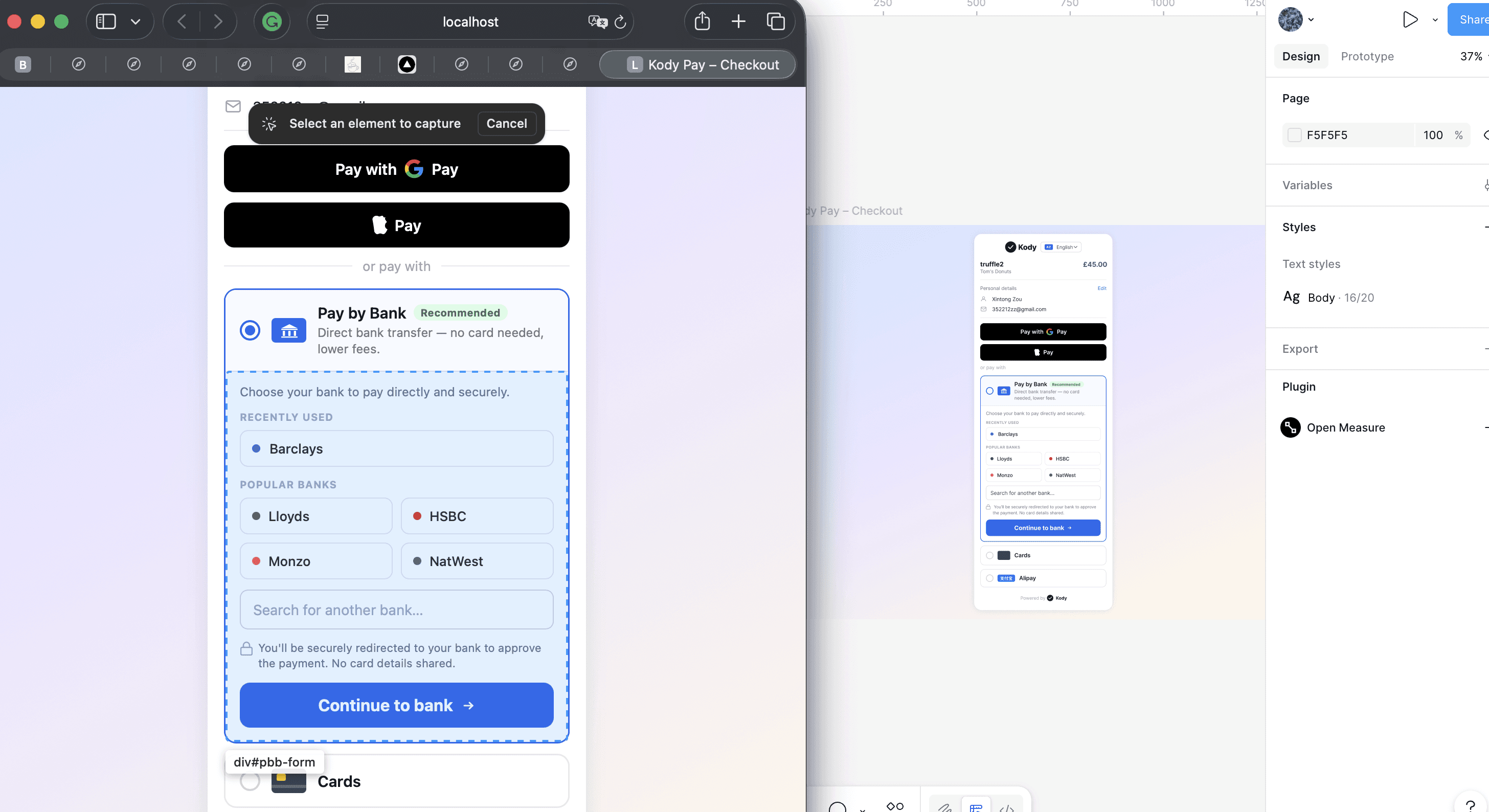

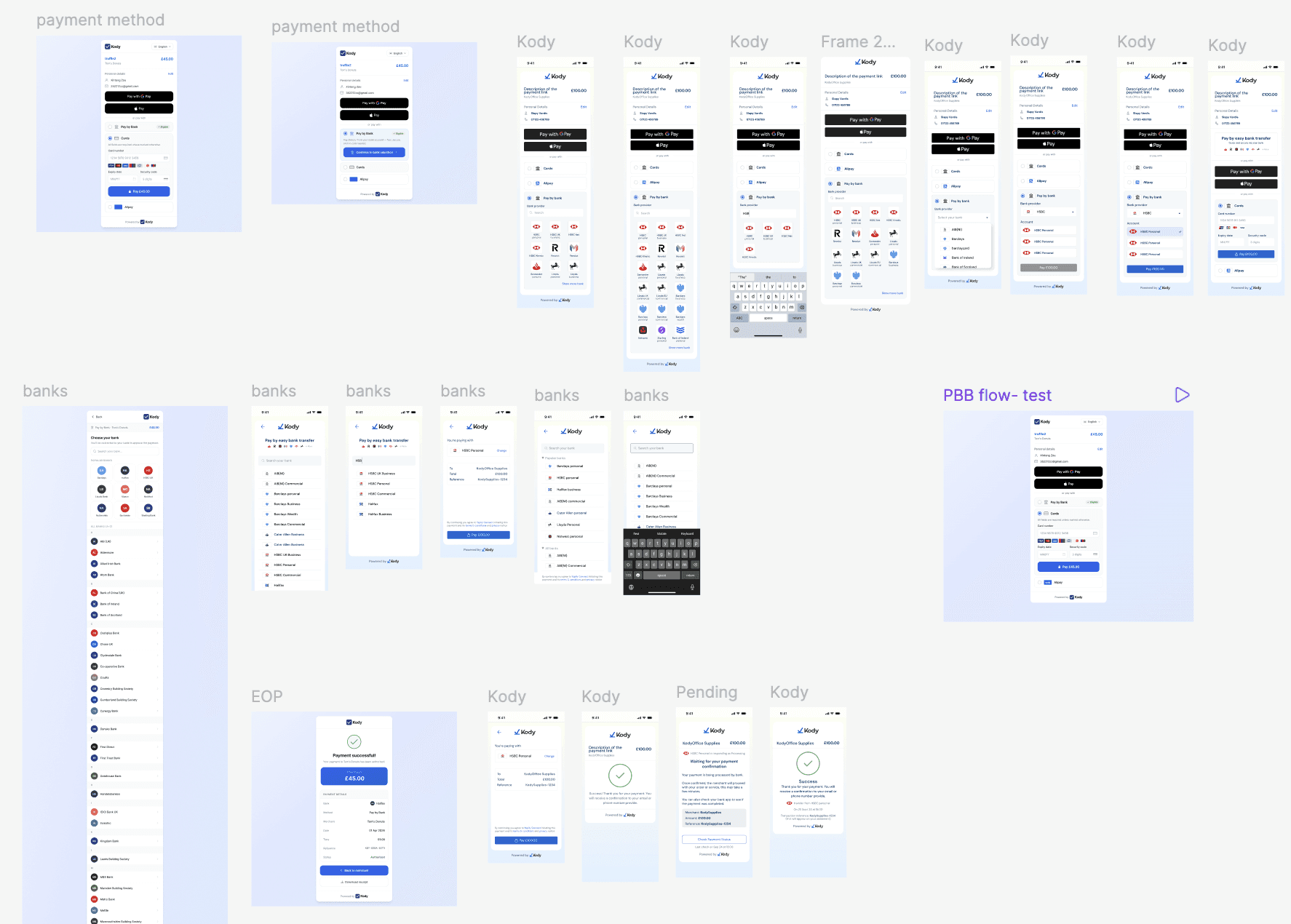

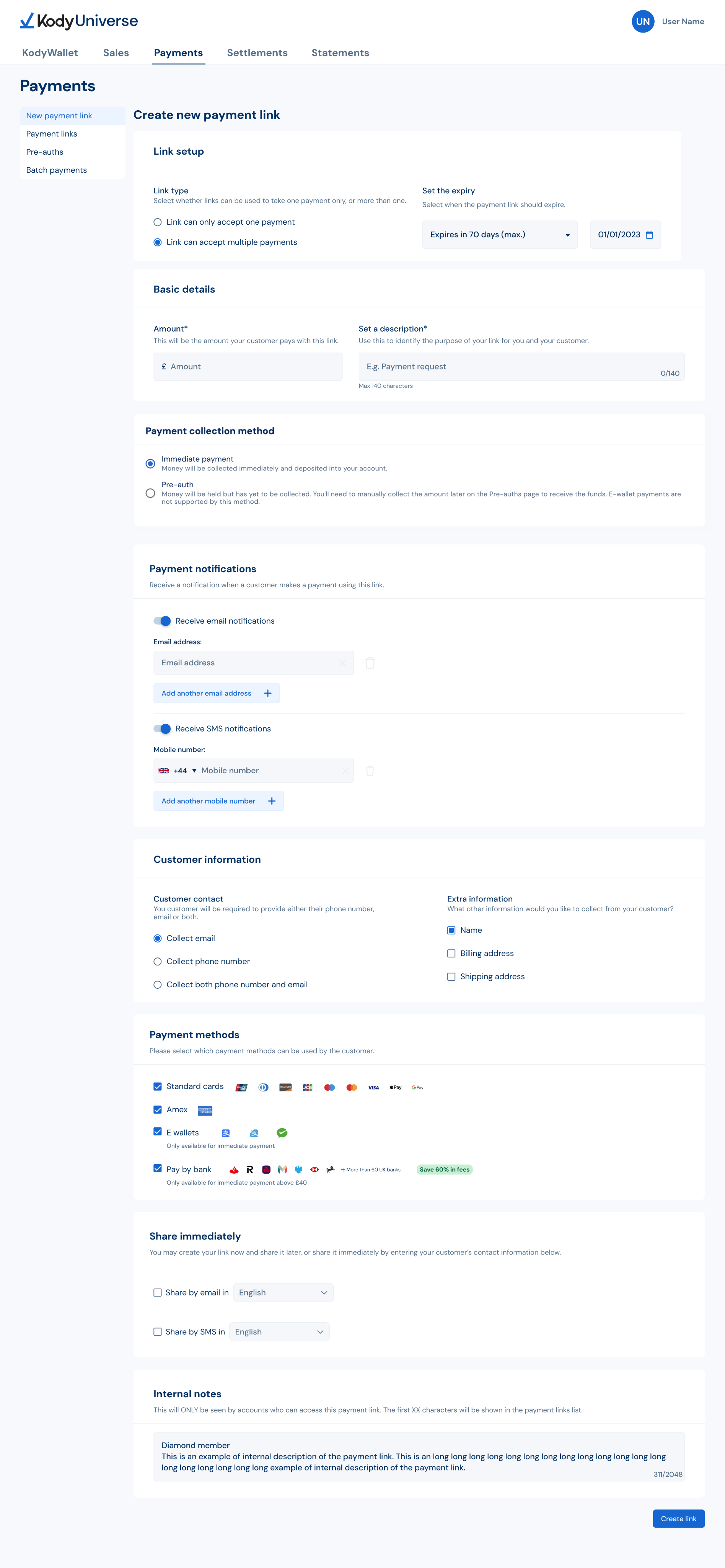

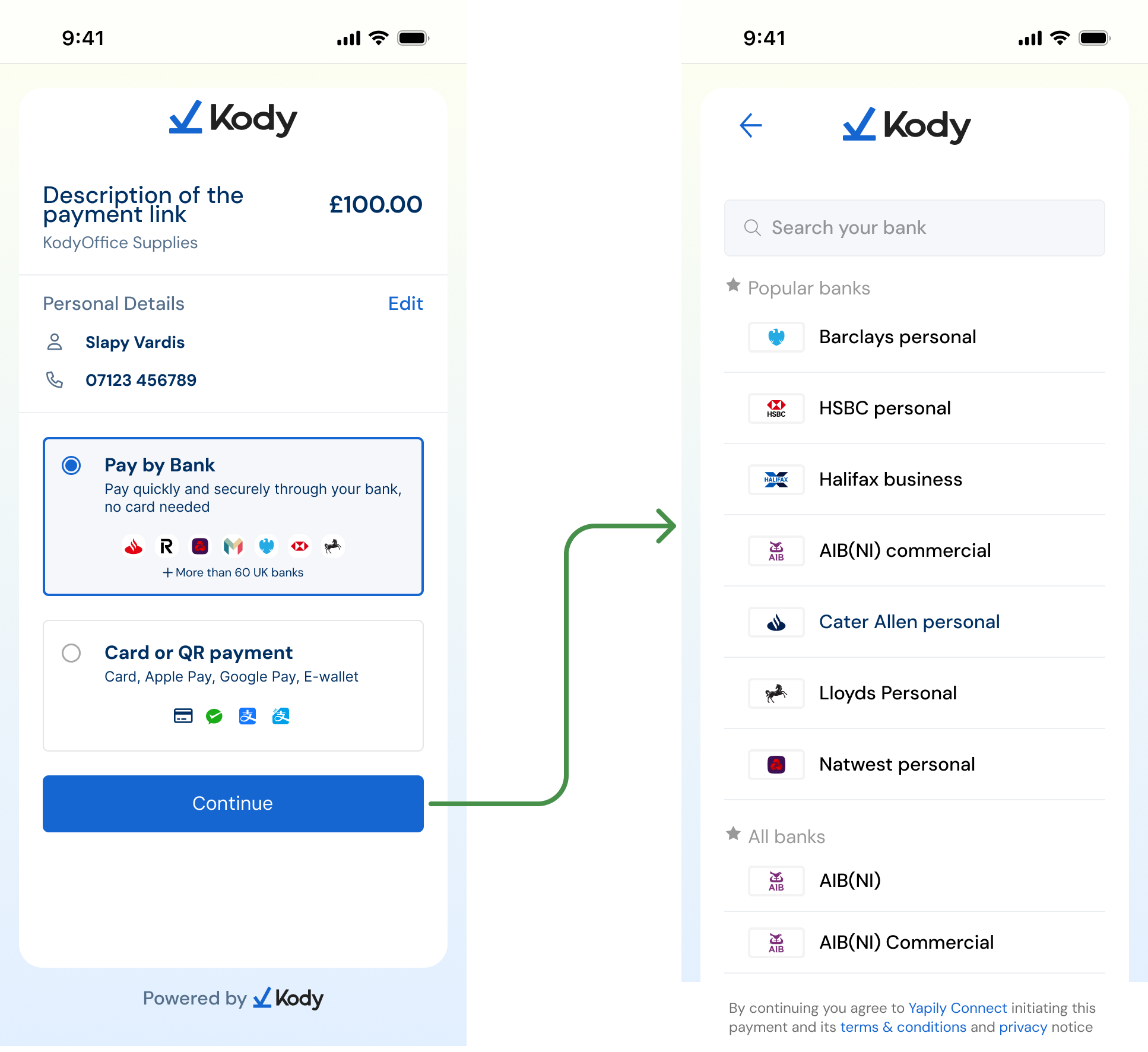

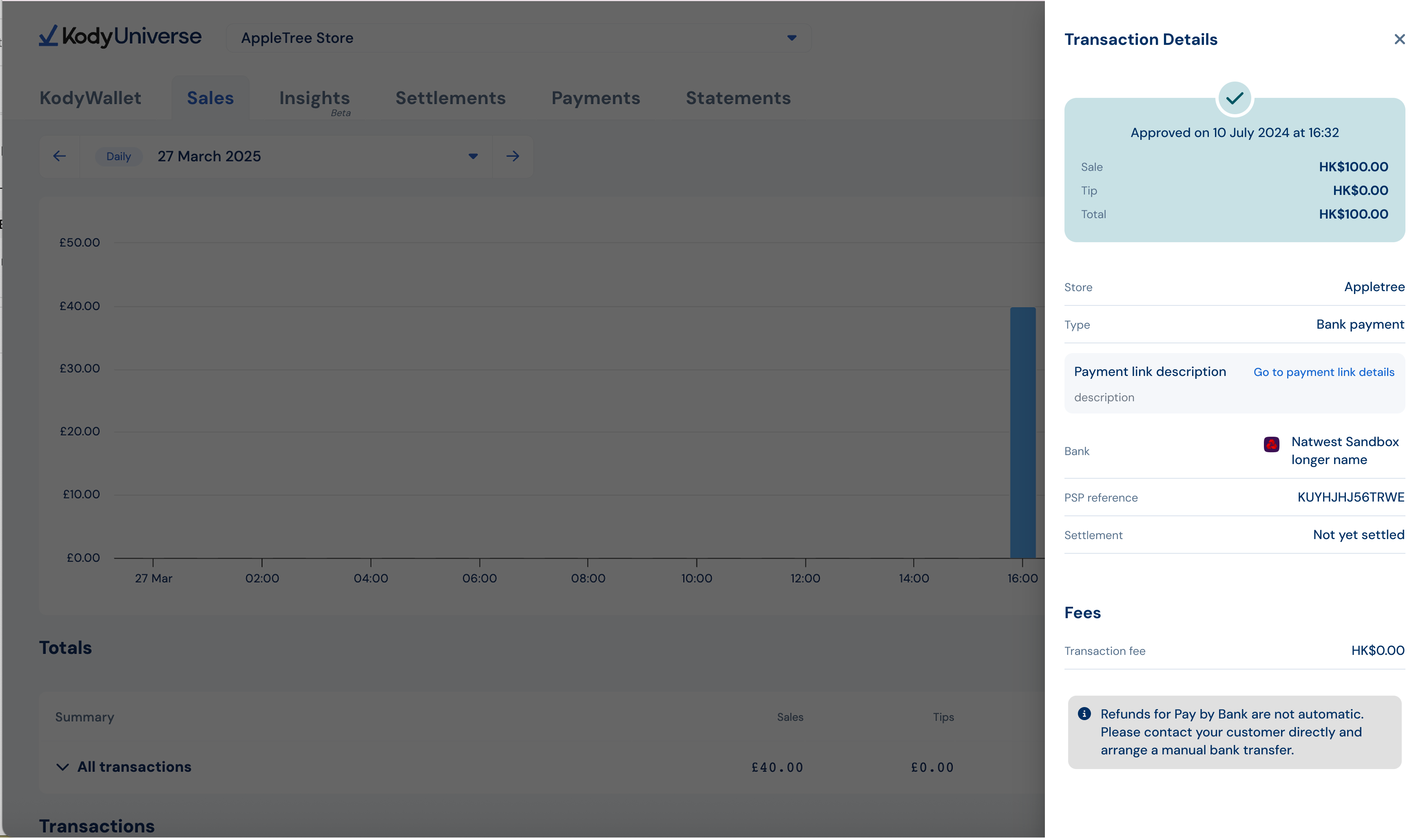

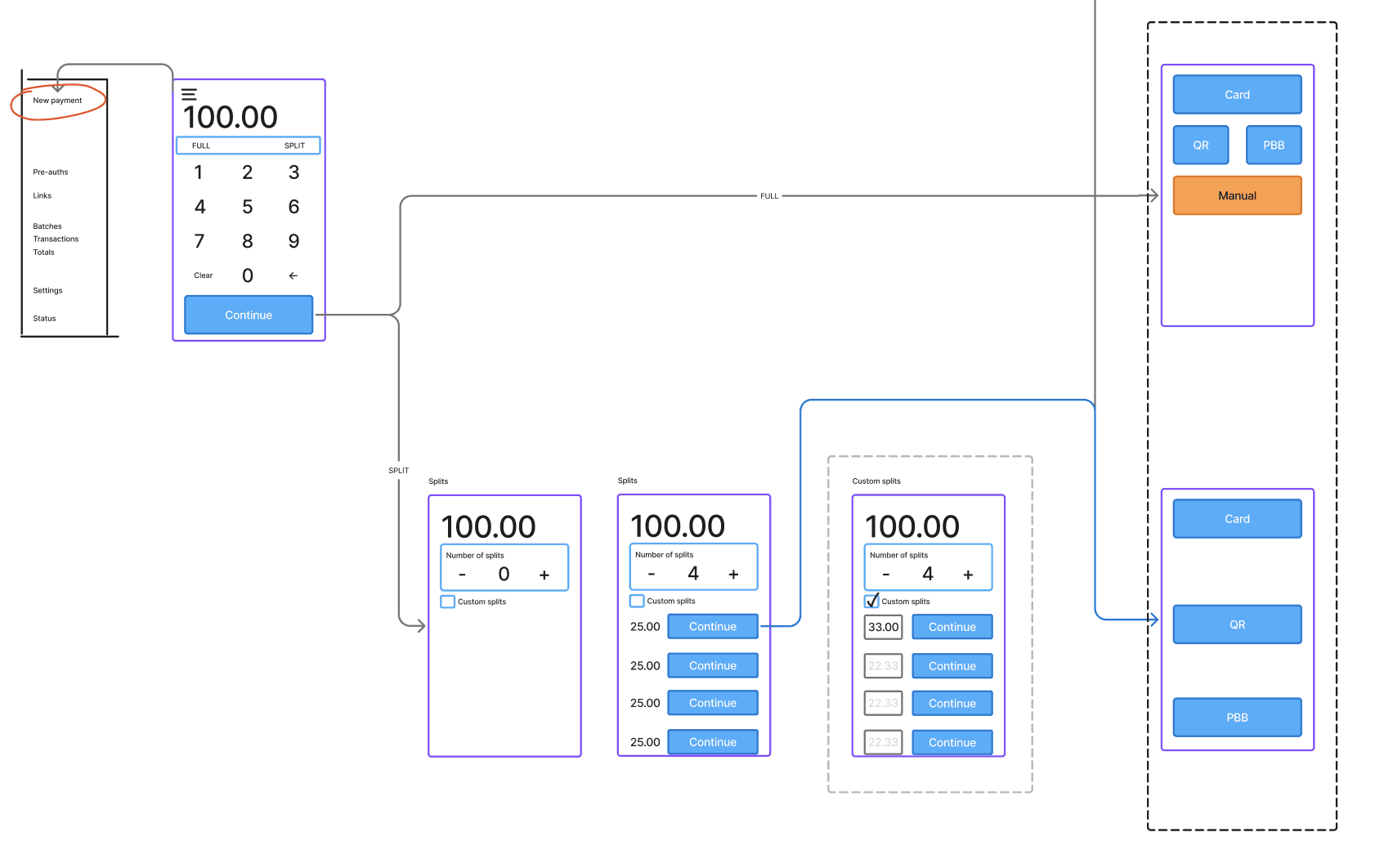

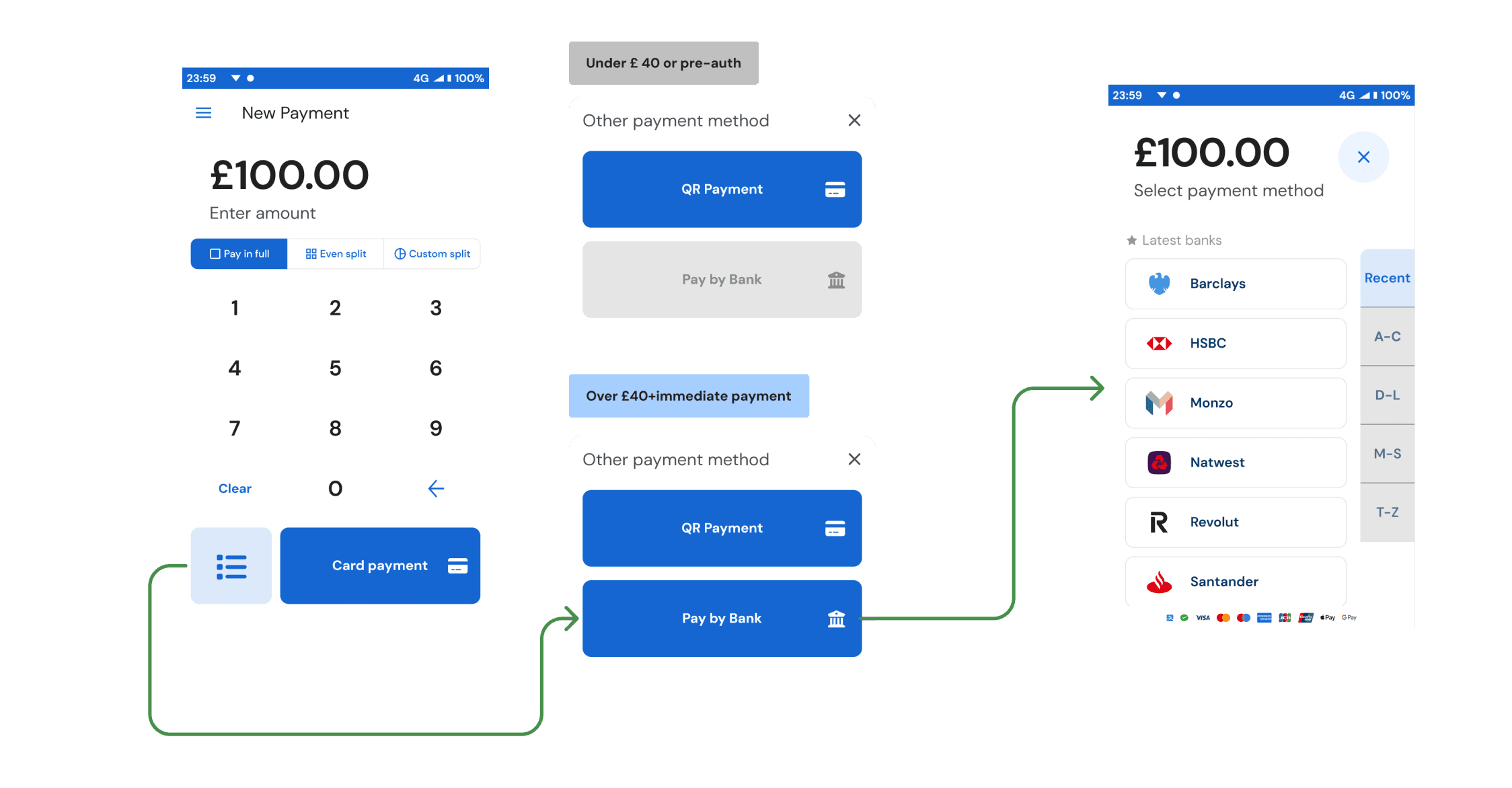

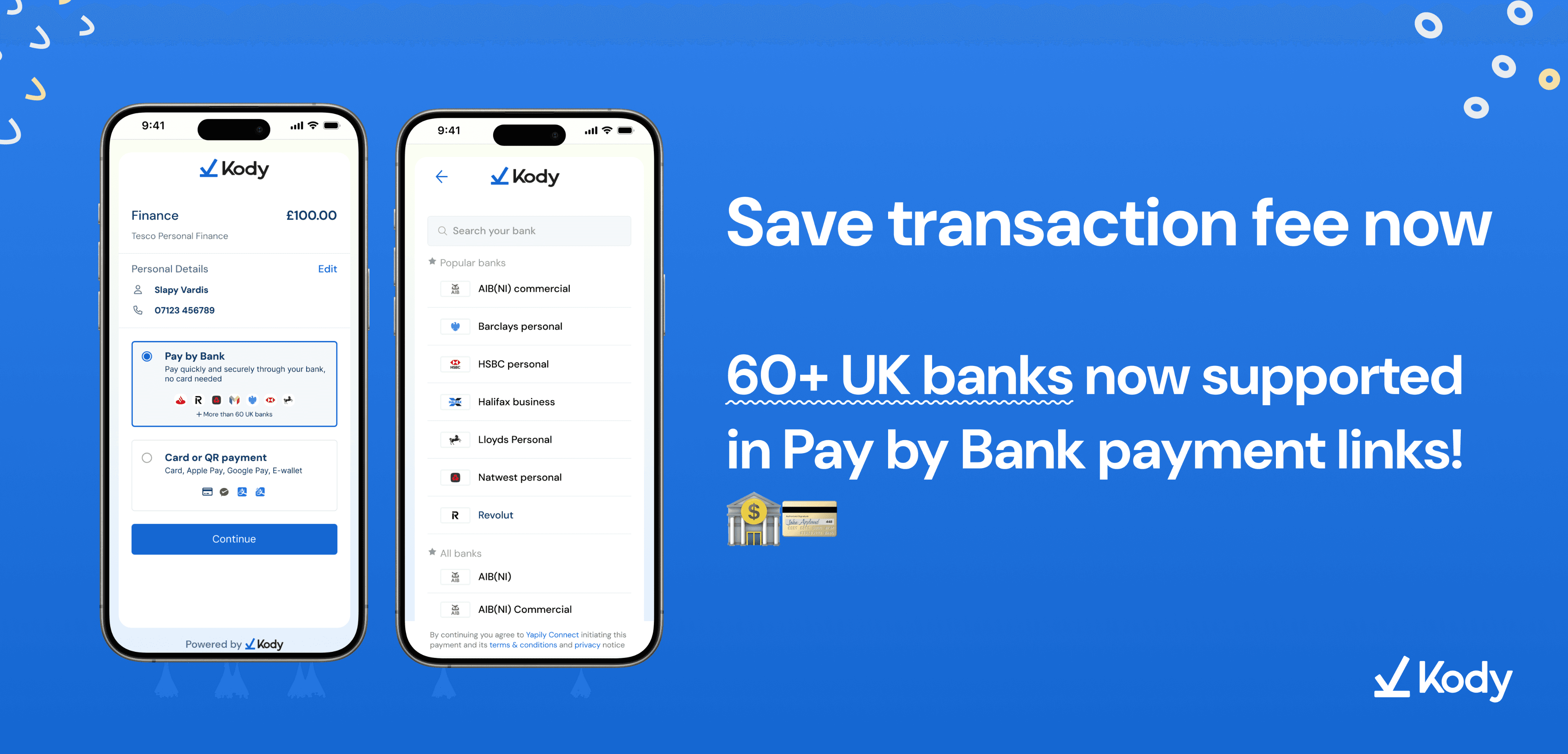

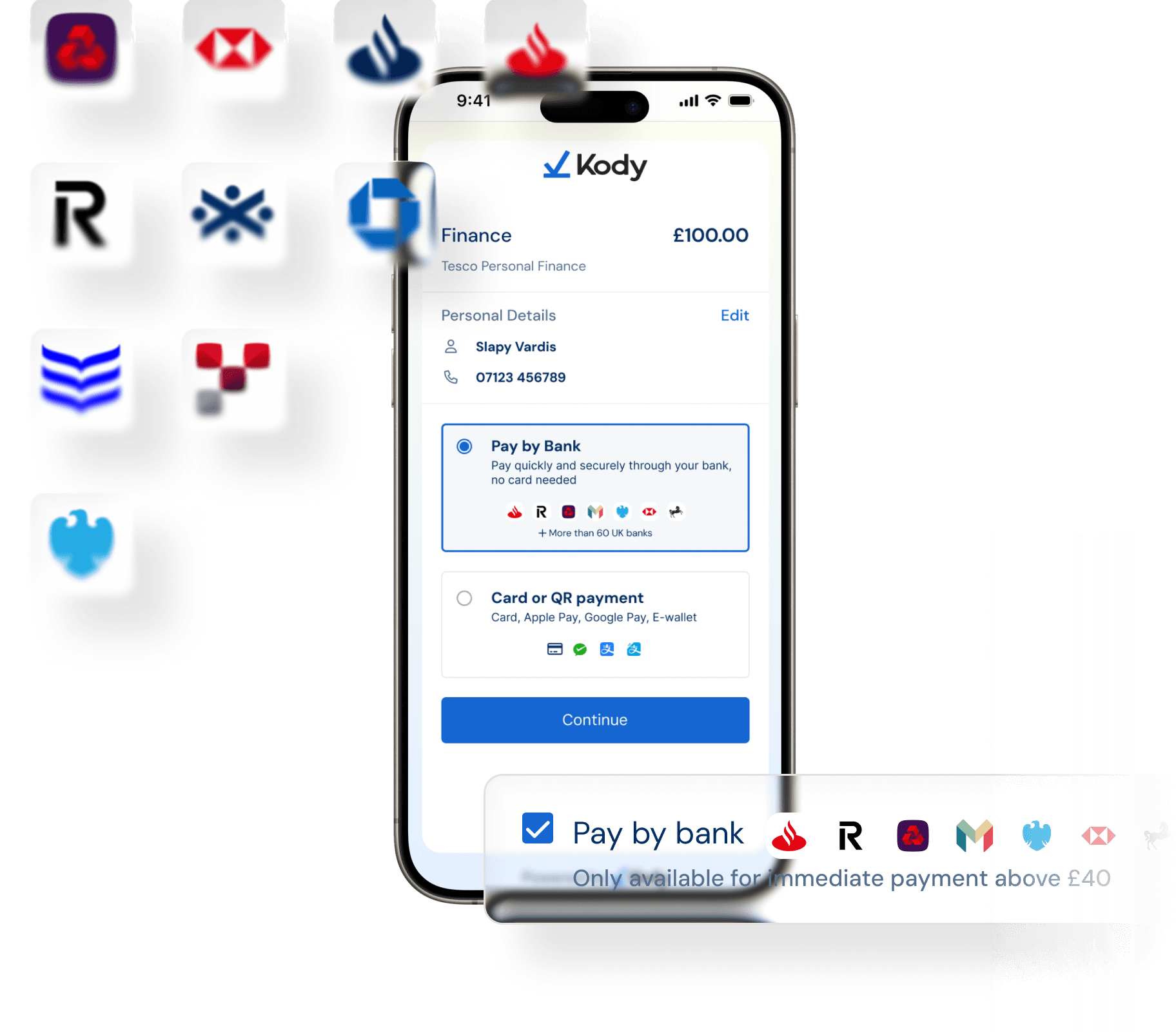

I led the redesign and adoption strategy for Kody's Pay by Bank (PBB) experience, an Open Banking payment method initially launched on in-person terminals.

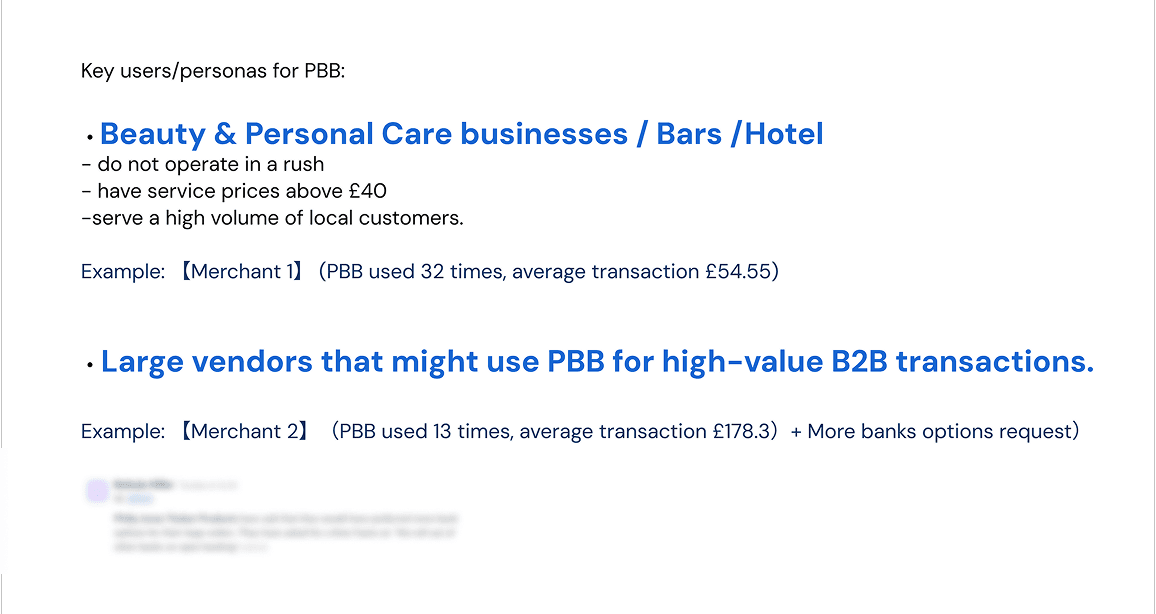

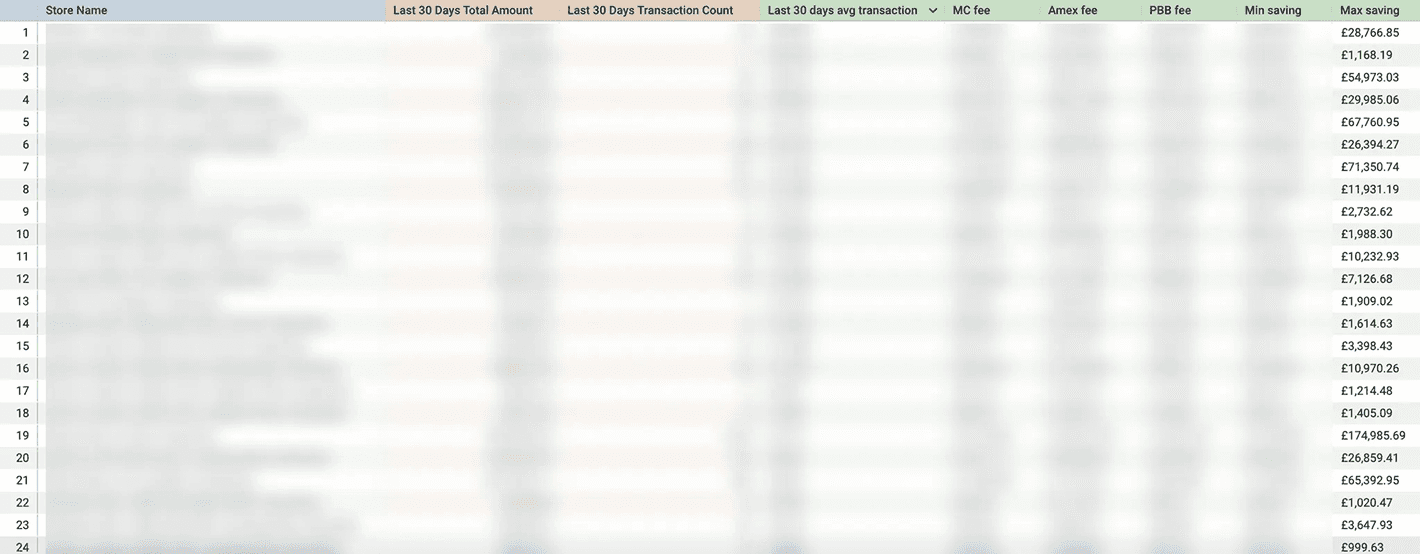

I reframed the problem, defined a persona aligned to a business needs and prioritised a new growth channel. The result was a ~120% usage uplift within a month, alongside increased payment-method share in eligible flows.

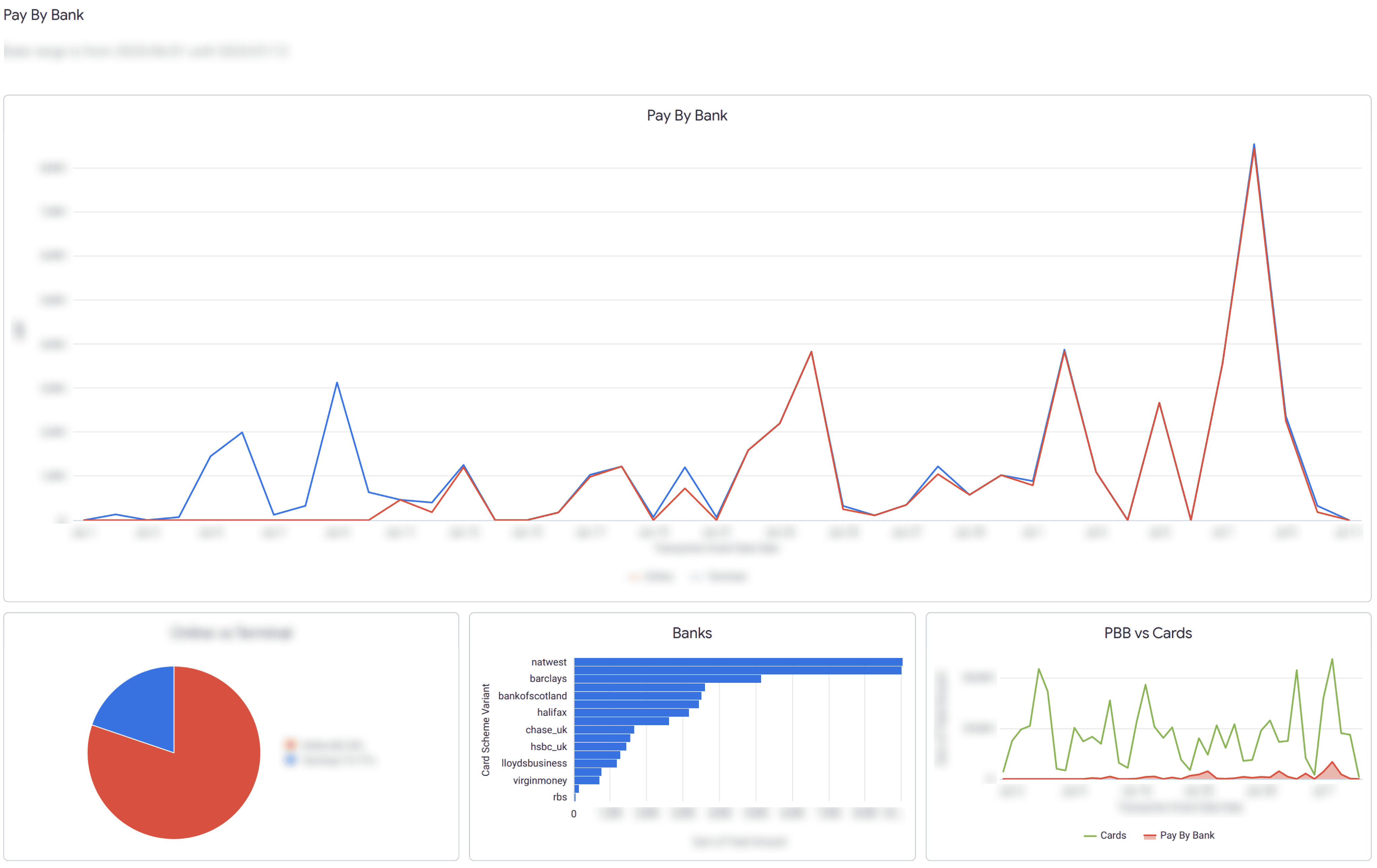

Starting from a request to add more banks to the terminal grid, I created lightweight prototypes to compare solution routes and conducted 10+ merchant and staff interviews to diagnose adoption blockers—channel fit.